Sven Van de Perre

Creative & Business Architect & Co-Founder, Tropos AR

By Lior Ronen | Founder, Finro Financial Consulting

Clearly understanding your business's worth and how it compares to competitors in the market is a powerful insight. It allows SaaS founders and executives to negotiate M&A deals or funding more effectively.

It lets employees and investors know how much their stocks or options could hypothetically be worth. It enables efficient communication with relevant stakeholders and elevates strategic discussions.

For SaaS (Software as a Service) businesses, this clarity is even more crucial due to their unique financial dynamics. At Finro, we prioritize three industry-standard valuation methods: Revenue Multiple, EBITDA Multiple, and Discounted Cash Flow (DCF). These methods are widely recognized for their effectiveness in assessing the true value of SaaS companies.

Revenue Multiple: This method involves multiplying the company's revenue by a specific multiple. It's a straightforward approach, especially useful for fast-growing SaaS businesses with robust revenue streams.

EBITDA Multiple: This method calculates the value based on earnings before interest, taxes, depreciation, and amortization (EBITDA). It provides insight into the company's profitability and operational efficiency.

Discounted Cash Flow (DCF): DCF valuation involves projecting the company's future cash flows and discounting them back to their present value. It's a comprehensive method that considers the company's growth potential and risk.

Valuing a SaaS business becomes crucial in various scenarios, such as seeking investment, planning an exit strategy, or understanding market position. Investors, company executives, and potential buyers rely on these valuations to make informed decisions.

This guide is designed to demystify these valuation methods and show you how to apply them effectively. This article will not make you a business valuation expert, but you'll have a solid understanding of how to accurately assess the value of your SaaS business, empowering you to navigate your financial future confidently.

Accurate revenue projections are crucial for any SaaS business's financial health and valuation. These projections guide your company's growth strategies and play a significant role in attracting investors and setting realistic financial goals.

In the context of SaaS company valuations, precise revenue forecasts provide a foundation for various valuation methods, including Revenue Multiple, EBITDA Multiple, and Discounted Cash Flow (DCF).

At Finro, revenue projection is the top priority in building a financial projection and valuation for a SaaS business, as it forms the basis for every financial exercise and is the first step in the valuation process.

Revenue projections guide the growth and financial success of SaaS companies. By setting achievable targets and identifying potential growth opportunities, they enable founders to allocate resources efficiently, prioritize initiatives, and adjust strategies based on projected performance. This planning is vital for maintaining a clear roadmap for future growth and ensuring that the business remains on track to meet its financial goals.

In addition to guiding internal strategies, accurate revenue projections are essential for attracting investors. Investors rely heavily on these forecasts to assess the potential return on their investment. Demonstrating a company's market potential and growth trajectory through precise revenue forecasts makes it more attractive to potential investors, facilitating the fundraising process and securing the necessary capital for expansion.

Revenue projections are also fundamental to the valuation process. Methods such as the Revenue Multiple and Discounted Cash Flow (DCF) rely directly on these forecasts to determine the company's worth. Accurate revenue projections ensure that the valuation reflects the true potential of the business, providing a realistic and reliable basis for negotiations during mergers and acquisitions or funding rounds.

Moreover, revenue projections provide critical insights for making informed strategic decisions about marketing, sales, product development, and customer support. By understanding which areas require more investment and identifying the strategies that drive growth, SaaS founders can make data-driven decisions that optimize their operations and enhance overall business performance.

In summary, revenue projections are the cornerstone of financial planning and valuation for SaaS businesses. They guide growth, attract investors, form the basis for valuation methods, and support strategic decision-making, ultimately driving the success and sustainability of the company.

Having established the importance of revenue projections, the next step is understanding the methods used to create these forecasts. There are several approaches, each with its own strengths and applicability depending on the stage and nature of the SaaS business.

Understanding the different revenue streams specific to SaaS businesses is crucial for building a comprehensive financial model. These streams contribute to the overall financial health and require accurate projection to ensure robust and reliable financial forecasts.

Subscription-Based Revenue: Customers pay a recurring fee for access to the software. This is the most common revenue stream for SaaS businesses and involves projecting the number of subscribers, pricing tiers, churn rates, and customer lifetime value (LTV).

Usage-Based Revenue: Customers pay according to their usage of the software or specific features. This requires estimating customer usage patterns and growth rates for each chargeable metric.

Freemium to Premium Conversion: A basic version of the software is offered for free, with advanced features available through a paid subscription. Forecasting involves estimating the number of free users, conversion rates to premium plans, and average revenue per premium user.

Professional Services: Additional services such as implementation, customization, training, or consulting. Revenue projections for these services involve estimating demand, pricing, and delivery capacity.

Add-Ons and Integrations: Additional features or third-party services that enhance the software. Forecasting involves estimating the percentage of customers purchasing these add-ons and the average revenue per sale.

With a clear understanding of the different revenue streams, we can now explore the methods used to project these revenues. Understanding these methods will help in choosing the right approach based on your business's stage, data availability, and specific needs.

At Finro, we use two primary methods for SaaS revenue forecasting: the TAM-SAM-SOM method and the User Journey method. Each method offers unique advantages and serves different purposes in the strategic planning of a SaaS startup.

Understanding these methods is crucial for selecting the most appropriate one based on the startup's stage, data availability, and specific needs.

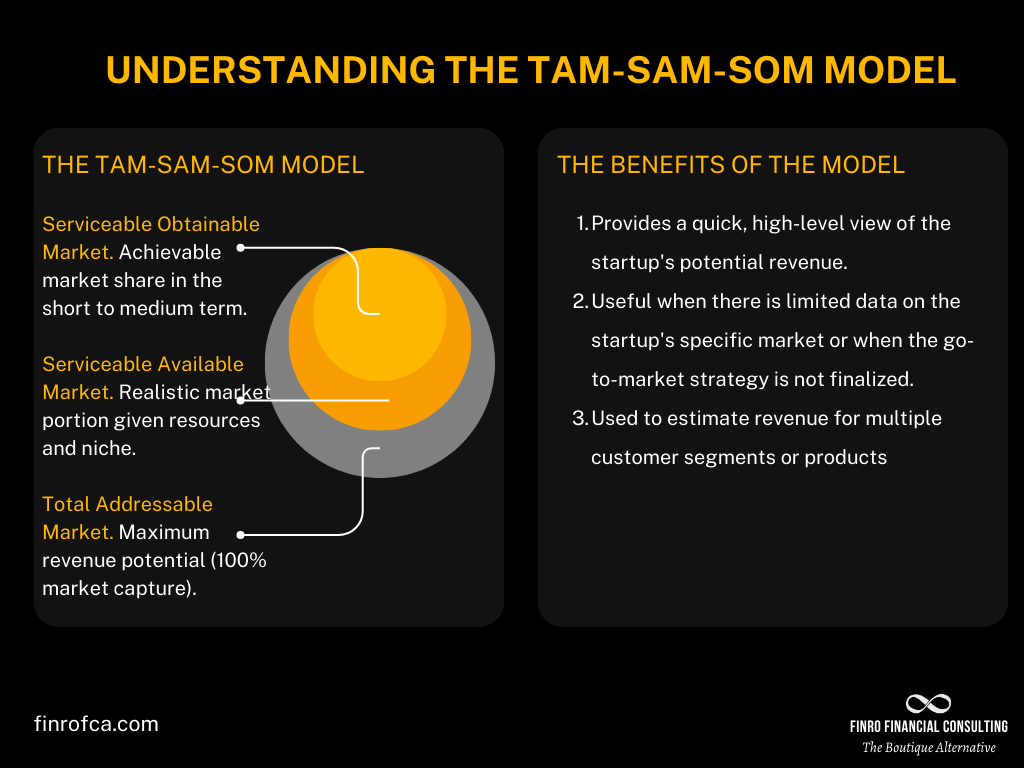

TAM-SAM-SOM Method

The TAM-SAM-SOM method, also known as the top-down approach, starts with a broad market perspective and narrows it down to more specific segments. It involves three key components:

Total Addressable Market (TAM): Represents the total revenue opportunity if the product were adopted by all potential customers globally.

Serviceable Available Market (SAM): The portion of TAM that is within your product’s reach, considering geographical and operational limitations.

Serviceable Obtainable Market (SOM): The fraction of SAM that your company can realistically capture given its competitive position, resource constraints, and market dynamics.

Strengths and Limitations

The TAM-SAM-SOM method is highly effective for assessing the overall market potential and setting a ceiling for achievable revenue. It is particularly useful for engaging investors, as it illustrates market opportunities during early funding rounds.

Additionally, it provides valuable strategic guidance for high-level planning and resource allocation based on market potential. However, this method may lack the detailed insights required for operational planning and execution. It often relies on broad assumptions, leading to overly optimistic forecasts.

When to Use The TAM-SAM-SOM Method

The TAM-SAM-SOM method is handy for early-stage startups that need to broadly assess market potential and evaluate the feasibility of their business concept. It communicates the overarching market opportunities to potential investors, providing essential insights during initial fundraising.

User Journey Method

The User Journey method dives deep into the specifics of customer interactions, tracking the path from initial awareness through engagement and conversion. It emphasizes a detailed analysis of each step in the sales funnel, incorporating real data to predict revenue more accurately.

Marketing Channel Budgeting: Allocating the marketing budget across various channels and analyzing conversion rates.

Conversion Percentages: Tracking how clicks convert to trials, demos, sign-ups, and paying customers.

Pricing Assumptions: Integrating different pricing strategies into the projections to see how they affect revenue.

Strengths and Limitations

The User Journey method leverages detailed, real-time data from customer interactions to provide highly accurate forecasts. This makes it highly relevant for operational strategies, highlighting effective touchpoints and potential bottlenecks in the customer journey. Moreover, it allows for dynamic adaptation, enabling ongoing adjustments to forecasts based on actual performance and customer behavior insights.

However, the method is data-dependent and requires access to detailed and reliable data, which may be challenging for early-stage startups without established sales and marketing processes. Additionally, it is more complex to implement and understand, requiring more resources and expertise in data analysis.

When to Use The User Journey Method

The User Journey method is best suited for more mature startups with access to detailed operational data. It becomes increasingly relevant as startups gain market traction, leveraging detailed data to create accurate and reliable revenue projections.

Startups that have achieved product-market fit and possess a comprehensive understanding of their target customers and sales channels should exclusively use the User Journey method for precise targeting and optimization of marketing and sales strategies.

By understanding the strengths and limitations of each method, SaaS founders can better align their forecasting efforts with their current business needs, ensuring both strategic direction and operational effectiveness.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a crucial financial metric for evaluating a company's operating performance and profitability.

Accurate EBITDA projections are essential for SaaS business valuation as they provide a clear picture of the company’s ability to generate earnings from its core operations. This section will explain what EBITDA is, how to calculate it, and provide a breakdown of a SaaS company's expenses into cost of revenues, payroll, and non-payroll expenses.

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is a measure of a company's overall financial performance and is used as an alternative to net income in some circumstances.

EBITDA focuses on the earnings generated from a company's core business operations by excluding the effects of financing, accounting decisions, and tax environments.

To calculate EBITDA, use the following formula:

EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

This formula adjusts net income by adding back interest, taxes, depreciation, and amortization expenses. By doing so, EBITDA provides a clearer view of a company's operating profitability and performance.

To accurately project EBITDA, it is essential to understand and categorize the expenses of a SaaS business. Finro breaks down these expenses into three main categories: cost of revenues, payroll, and non-payroll operating expenses.

Cost of Revenues or Cost of Goods Sold (COGS)

Cost of revenues, also known as Cost of Goods Sold (COGS), includes all direct costs associated with producing and delivering a SaaS product. This encompasses expenses such as cloud infrastructure costs, customer support, sales commissions, and any fees related to delivering the service.

Unlike traditional COGS, which focuses solely on production costs, the cost of revenues provides a broader perspective by incorporating additional expenses necessary for generating revenue. For SaaS companies, these costs are crucial as they directly impact the gross margin and overall profitability.

Payroll Expenses

Payroll expenses are a significant component of operating costs for SaaS businesses. This includes salaries, bonuses, stock-based compensation, and sales commissions for all employees. At Finro, payroll forecasting involves a multi-step approach to accurately project future payroll expenses.

It begins with mapping current headcount and projecting future personnel requirements based on the product roadmap. This involves estimating the timing and number of new hires and considering both direct and indirect impacts of expanding the company's headcount. Accurate payroll forecasting is essential for understanding the financial implications of hiring decisions and ensuring sustainable growth.

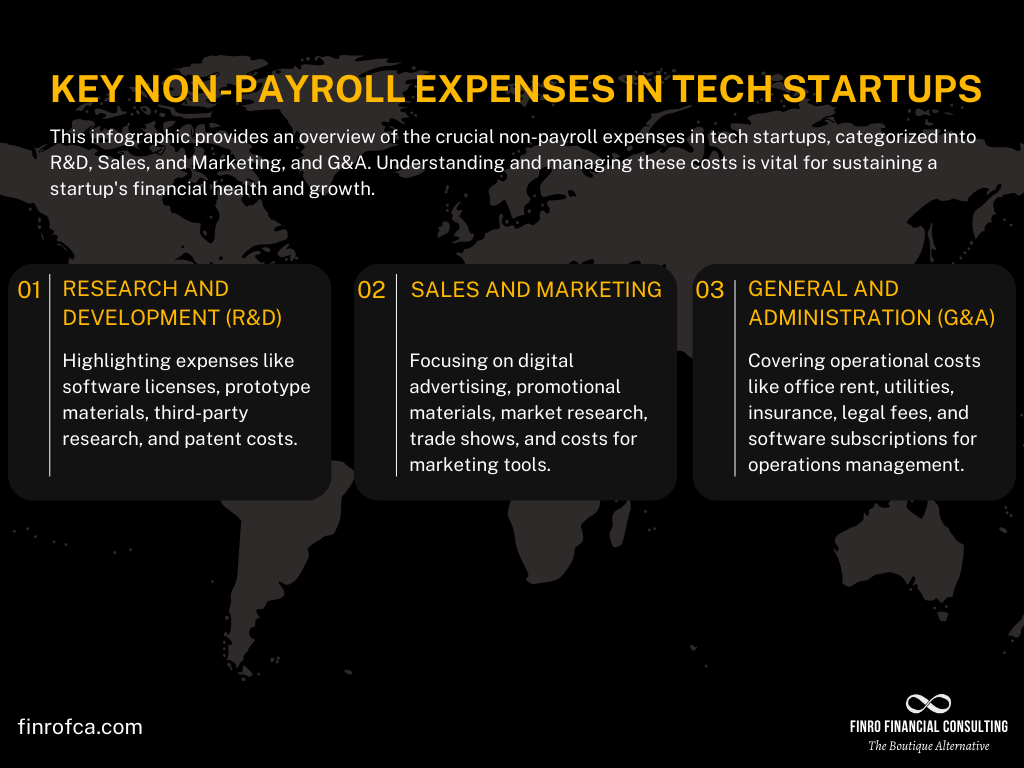

Non-Payroll Operating Expenses

Non-payroll operating expenses cover a wide range of costs that are not directly tied to employee salaries or the production of goods. These expenses are typically categorized into Research and Development (R&D), Sales and Marketing, and General and Administrative (G&A).

R&D expenses include costs related to developing new products or services and improving existing ones, such as software licenses, prototype materials, and patent filing fees. Sales and marketing expenses encompass digital advertising, promotional materials, market research, and software tools used in marketing. G&A expenses cover operational costs necessary to run the business, such as office rent, utilities, insurance, legal and professional fees, and software subscriptions for operations management. Effectively managing non-payroll expenses is crucial for maintaining financial health and ensuring that resources are allocated efficiently.

By understanding and accurately forecasting these expense categories, SaaS businesses can develop more reliable EBITDA projections, providing a realistic view of their profitability and supporting strategic decisions.

Forecasting EBITDA for a SaaS business requires a blend of historical analysis and forward-looking considerations.

The goal is to create projections reflecting past performance and future expectations, ensuring they align with revenue projections and strategic goals.

Historical Trends: Analyzing historical financial data is the first step in forecasting EBITDA. This involves examining past income statements to identify trends in revenue, cost of revenues, payroll, and non-payroll operating expenses. By understanding these historical patterns, businesses can establish a baseline for future projections.

Key considerations include:

Past Revenue Growth: Assessing how revenue has grown over time and identifying factors influencing this growth.

Expense Trends: Analyzing how different expense categories have changed in relation to revenue growth.

Profitability Metrics: Reviewing historical EBITDA margins to understand the relationship between revenue and operating expenses.

Future Milestones and Events: Besides historical trends, it is crucial to factor in future milestones and events that could impact expenses. These might include planned product launches, market expansions, hiring initiatives, or strategic investments. Each event can influence various cost categories and, consequently, EBITDA.

For example:

Product Development: Forecasting increased R&D expenses for new product launches.

Market Expansion: Projecting higher sales and marketing costs to enter new markets.

Hiring Plans: Estimating payroll growth based on headcount expansion aligned with the product roadmap.

The assumptions used to forecast costs and EBITDA should align closely with revenue projections. If revenue is expected to grow significantly, corresponding increases in cost of revenues, payroll, and non-payroll expenses should be anticipated. This alignment ensures the projections are realistic and reflect the company’s operational strategy.

Revenue Growth Assumptions: Align cost growth assumptions with projected revenue growth to maintain consistent profit margins.

Scalability Considerations: Consider how economies of scale might impact cost efficiency as the business grows.

Strategic Initiatives: Ensure that strategic goals, such as entering new markets or launching new products, are reflected in both revenue and cost projections.

SaaS businesses can create accurate and strategic EBITDA forecasts by combining historical trends with future milestones and aligning these with revenue projections. This approach ensures that financial projections are based on past performance and geared toward achieving future business objectives.

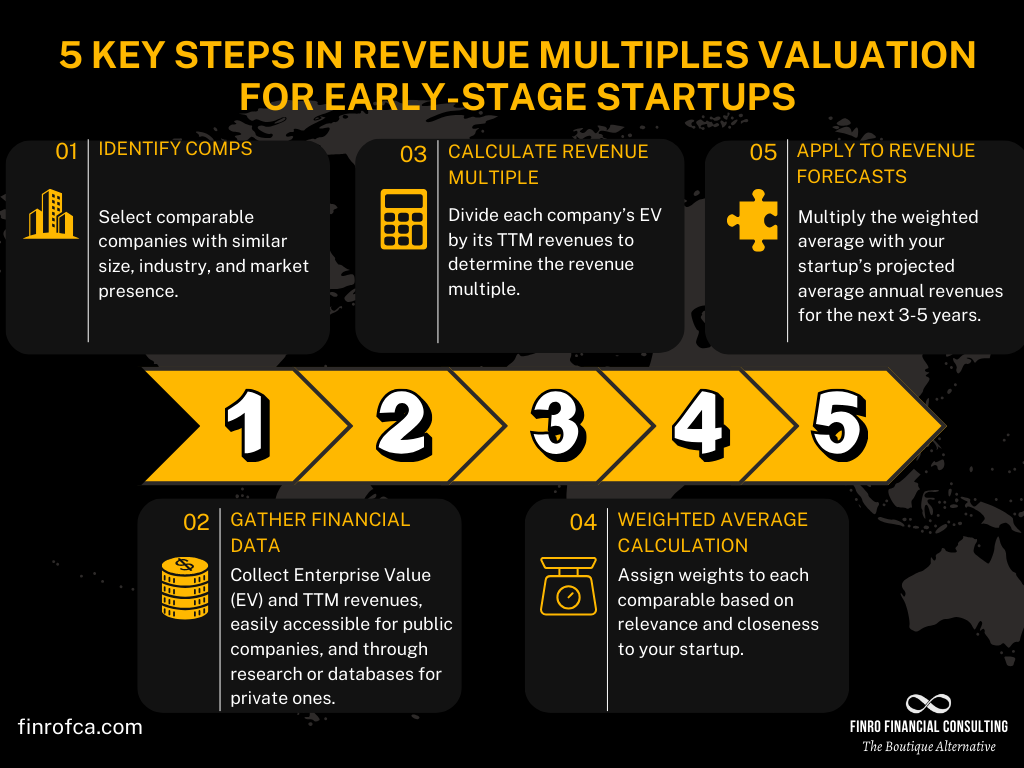

The Revenue Multiple method is a commonly used valuation approach, especially for SaaS businesses. It involves valuing a company based on its revenue, using a specific multiple derived from comparable companies or industry standards.

This method is particularly useful for businesses with predictable and strong revenue streams, providing a straightforward way to estimate the company's enterprise value.

Calculating the Revenue Multiple involves multiplying the company's total revenue by an industry-specific multiple. This multiple reflects how much investors are willing to pay for each dollar of revenue, considering factors such as growth potential, market conditions, and risk profile.

Formula:

Enterprise Value (EV) = Revenue × Revenue Multiple

For example, if a SaaS company generates $10 million in annual revenue and the industry revenue multiple is 5, the enterprise value would be EV = $10 million × 5 = $50 million.

Several factors can influence the revenue multiple assigned to a SaaS business:

Growth Rate: Companies with higher revenue growth rates typically command higher valuation multiples, reflecting their potential for future expansion.

Market Conditions: Favorable market conditions, such as increasing demand for SaaS solutions or overall economic growth, can positively impact the revenue multiple.

Competitive Landscape: The presence of strong competitors or barriers to entry in the market can affect the multiple. A dominant market position often results in a higher multiple.

Profitability: While the revenue multiple primarily focuses on revenue, underlying profitability can still influence investor perceptions and, consequently, the multiple.

Customer Metrics: High customer retention rates and low churn rates indicate a stable revenue stream, potentially increasing the revenue multiple.

Operational Efficiency: Efficient operations that lead to higher gross margins and controlled operating expenses can positively impact the multiple.

Pros:

Simplicity: The Revenue Multiple method is straightforward and easy to apply, making it accessible for various stakeholders.

Focus on Growth: It emphasizes revenue growth, which is often a primary driver of value for SaaS companies.

Comparable Analysis: This method allows for easy comparison with other companies in the industry, providing a benchmark for valuation.

Cons:

Ignores Profitability: The method does not consider a company’s profitability, which can be a significant oversight, especially for businesses with high expenses relative to revenue.

Market Volatility: Revenue multiples can fluctuate with market conditions, leading to potential overvaluation or undervaluation in volatile markets.

Lack of Granularity: This approach may oversimplify the valuation process by not accounting for other important financial metrics and operational aspects.

The Revenue Multiple method offers a practical way to estimate the value of a SaaS business based on its revenue. While it provides valuable insights, it is essential to consider its limitations and use it in conjunction with other valuation methods for a more comprehensive assessment.

The EBITDA Multiple method is another common valuation approach used for SaaS businesses. It involves valuing a company based on its EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), using a specific multiple derived from comparable companies or industry standards.

This method provides a clearer picture of a company’s operational profitability by excluding non-operational expenses and non-cash items.

Calculating the EBITDA Multiple involves multiplying the company's EBITDA by an industry-specific multiple. This multiple reflects how much investors are willing to pay for each dollar of EBITDA, considering factors such as operational efficiency, growth potential, and market conditions.

Formula:

Enterprise Value (EV) = EBITDA × EBITDA Multiple

For example, if a SaaS company generates $5 million in EBITDA and the industry EBITDA multiple is 8, the enterprise value would be: EV = $5 million × 8 = $40 million.

Several factors can influence the EBITDA multiple assigned to a SaaS business:

Operational Efficiency: Companies with higher operational efficiency, reflected in strong EBITDA margins, typically command higher multiples.

Growth Rate: Higher growth rates in EBITDA suggest strong future performance, leading to higher multiples.

Market Conditions: Favorable economic and market conditions can positively impact the EBITDA multiple.

Competitive Landscape: A strong competitive position can lead to higher multiples, indicating a more defensible business model.

Revenue Quality: Predictable, recurring revenue streams with high customer retention rates can increase the multiple.

Debt Levels: Lower debt levels can result in higher multiples, indicating lower financial risk.

Pros:

Focus on Operational Performance: The EBITDA Multiple method focuses on the company's operational profitability, providing a clearer view of core business performance.

Excludes Non-Cash Items: By excluding non-cash expenses like depreciation and amortization, the company's cash-generating ability is better understood.

Comparability: It allows for easy comparison with other companies in the industry, offering a benchmark for valuation.

Cons:

Ignores Capital Structure: The method does not account for differences in capital structure, which can impact overall financial health.

Excludes Interest and Taxes: By excluding interest and taxes, it may overlook important financial performance and risk aspects.

Market Volatility: Like revenue multiples, EBITDA multiples can fluctuate with market conditions, potentially leading to overvaluation or undervaluation.

The EBITDA Multiple method is a valuable tool for assessing the value of a SaaS business based on its operational profitability.

While it provides critical insights into core business performance, it should be used alongside other valuation methods to obtain a comprehensive view of the company's value.

The Discounted Cash Flow (DCF) method is a valuation approach that estimates the value of a company based on its future cash flows. This method involves projecting the company’s cash flows over a certain period and then discounting them back to their present value using an appropriate discount rate.

The DCF method provides a comprehensive view of a company's intrinsic value by considering its future earning potential and the time value of money.

Calculating the DCF involves several steps:

Project Future Cash Flows: Estimate the company’s free cash flows for a specific forecast period, typically 5-10 years.

Determine the Terminal Value: Estimate the value of the company beyond the forecast period, often using a perpetuity growth model or an exit multiple.

Calculate the Discount Rate: Determine the discount rate, commonly the company's weighted average cost of capital (WACC), which reflects the riskiness of the cash flows.

Discount the Cash Flows: Discount the projected cash flows and terminal value back to their present value using the discount rate.

Sum the Present Values: Add the present values of the projected cash flows and terminal value to get the total enterprise value.

Formula:

DCF Value = ∑(Cash Flowt(1+r)t) + Terminal Value (1+r)n

Where:

Cash Flow t = Cash flow in year t

r = Discount rate (WACC)

n = Number of years in the forecast period

Several factors can influence the DCF valuation of a SaaS business:

Accuracy of Cash Flow Projections: The reliability of the DCF method depends heavily on the accuracy of the projected cash flows.

Discount Rate: The chosen discount rate, reflecting the company’s risk profile, significantly impacts the present value of future cash flows.

Terminal Value Assumptions: The assumptions used to estimate the terminal value, such as growth rates or exit multiples, can greatly affect the overall valuation.

Market Conditions: Economic and market conditions can influence the discount rate and growth assumptions, affecting the valuation.

Business Performance: The company's operational performance, including revenue growth, margin expansion, and cost control, directly impacts projected cash flows.

Pros:

Comprehensive Analysis: The DCF method provides a detailed and comprehensive view of a company's value by considering its future earning potential.

Intrinsic Value Focus: It focuses on the intrinsic value of the business, independent of market conditions.

Flexibility: The method can be tailored to reflect various scenarios and assumptions, offering a range of potential outcomes.

Cons:

Complexity: The DCF method is complex and requires detailed financial projections and assumptions, which can be challenging to develop accurately.

Sensitivity to Assumptions: Small changes in assumptions, such as the discount rate or terminal value growth rate, can significantly impact the valuation.

Data-Intensive: It requires a substantial amount of data, which may not be readily available for all businesses, especially startups.

The DCF method is a powerful tool for valuing a SaaS business by focusing on its future cash flow generation and intrinsic value. While it offers a thorough and flexible approach, its accuracy depends on the reliability of the underlying assumptions and projections.

Using the DCF method in conjunction with other valuation approaches can provide a more rounded and robust assessment of a company's value.

Sven Van de Perre

Creative & Business Architect & Co-Founder, Tropos AR

Tropos AR worked with Finro, at the start of the Web3 boom. They where one of the very few companies that had a correct view of the leap in technology, which is now slowly unfolding.

Technology always gets overvalued in the short-term, and undervalued in the long term.

And Finro helped us navigate that future like few others can.

Startups at different stages of development exhibit varying financial performances, business model stabilities, and growth potentials.

Depending on these factors, the appropriate valuation method can differ significantly.

Here, we explore the most suitable valuation methods for startups at different stages.

Super early-stage startups are characterized by their nascent business development. Typically, these companies are pre-revenue, working on proof of concept or early stages of product development. They often have a rough idea of their business model and monetization strategy, but much remains untested.

In these stages, startups usually do not need a formal valuation. Instead, they can finance their operations through bootstrapping, small bank loans, or unpriced rounds using instruments like SAFEs (Simple Agreements for Future Equity) or convertible notes. These mechanisms allow startups to raise funds without immediately determining a precise valuation.

Unpriced Rounds:

SAFE: An investment tool that gives investors the right to future equity without accruing interest or having a maturity date.

Convertible Note: A short-term debt that converts into equity at the next financing round, accruing interest over time and having a maturity date.

In the pre-seed and seed stages, startups may begin to see more structured development but are still early in their journey. These companies might be in the pre-alpha or alpha stage of product development with some clarity on their business model and monetization plan. Funding rounds at these stages often include angel investors, accelerators, or micro-VCs.

Valuation methods for these stages include both qualitative and quantitative approaches:

Qualitative Methods:

Berkus Method: Evaluates the startup based on qualitative aspects such as the management team, market potential, and product development stage.

Risk Factor Summation Method: Assesses various risk factors to adjust the valuation positively or negatively.

Payne Scorecard Method: Scores the startup based on key criteria like the strength of the idea, market size, and competitive environment.

Quantitative Methods:

Venture Capital (VC) Method: Estimates the startup’s future value at exit and works backwards to determine the current valuation.

Comparables Method: Uses revenue forecasts and revenue multiples from similar companies to derive a valuation.

At Series A and B stages, startups are more mature with products often in late alpha, beta, or even MVP stages. They have clearer insights into their business models, monetization plans, and user acquisition strategies. These startups can make more accurate financial and business projections.

Valuation methods typically used at this stage include:

Comparables Method: This involves using revenue multiples, and if applicable, EBITDA multiples from similar companies to value the startup.

Revenue Multiple Method: Focuses on applying industry-specific revenue multiples to the startup's revenue projections.

If the company has reached EBITDA profitability, the EBITDA multiples are included in the analysis to provide a more comprehensive valuation.

Late-stage startups are much more mature, with a clear path to profitability and a solid understanding of their market and customer base. They have substantial financial and business data, making them suitable for more sophisticated valuation methods.

Investors at this stage include late-stage venture capital firms, private equity funds, and family offices. These investors use a mix of valuation methods to ensure accuracy and reduce biases:

Comparables Method: Continues to be a primary method, applying both revenue and EBITDA multiples.

Discounted Cash Flow (DCF) Method: Projects the company’s future cash flows and discounts them to present value using the weighted average cost of capital (WACC).

Net Asset Value (NAV) Method: Used if the startup has significant revenue-generating assets, valuing each asset separately and aggregating the total.

Choosing the right valuation method depends heavily on the startup's stage, available data, and specific circumstances. Early-stage startups often rely on qualitative methods and unpriced rounds, while more mature startups use quantitative methods like comparables and DCF.

Understanding and applying the appropriate valuation method for each stage is crucial for both founders and investors to make informed decisions. This tailored approach to valuation aligns with the startup's current state and future potential, facilitating strategic growth and investment.

| Stage | Characteristics | Valuation Methods |

|---|---|---|

| Idea to Pre-Seed | Idea validation, proof of concept, pre-revenue. | Unpriced rounds (SAFE, Convertible Notes), no immediate need for valuation. |

| Pre-Seed and Seed | Initial development, possibly pre-alpha/alpha stage, clarity on business model. | Qualitative methods (Berkus, Risk Factor Summation, Payne Scorecard) for angels; Quantitative methods (Venture Capital Method, Comparables) for VCs. |

| Series A and B | Late stage of alpha/beta, possibly MVP, finding product-market fit, beginning to understand business model. | Comparables method (revenue and EBITDA multiples), more structured financial and business projections. |

| Series C to Beyond | Mature startups, clear path to profitability, substantial business and financial data. | Comparables, Discounted Cash Flow (DCF), Net Asset Value (NAV), multiple methods for accuracy and bias reduction. |

Valuing a SaaS business accurately requires understanding and analyzing several key metrics that reflect the company's financial health, operational efficiency, and growth potential.

These metrics provide insights into various business aspects, from revenue generation and customer retention to cost management and profitability.

This section will discuss the essential metrics to consider when valuing a SaaS business, focusing on MRR, ARR, ACV (for B2B SaaS), ARPU, CAC, LTV, churn rate, conversion rate, and gross margin.

Monthly Recurring Revenue (MRR): MRR is the predictable revenue that a SaaS business can expect to receive every month. It includes subscription fees, recurring add-ons, and any recurring usage fees. MRR is crucial for understanding the company’s revenue stability and growth trajectory.

Annual Recurring Revenue (ARR): ARR is the annualized version of MRR, providing a broader view of the company’s revenue on a yearly basis. ARR is particularly useful for long-term planning and assessing the overall health of the subscription business. Both MRR and ARR are fundamental for evaluating the revenue stability and growth potential of a SaaS business.

Average Contract Value (ACV): ACV is a key metric for B2B SaaS businesses that measures the average annual revenue per customer contract. It helps in understanding the value of each customer and the impact of contract length and size on overall revenue.

ACV = Total Annual Revenue from Contracts / Number of Contracts

ACV is essential for assessing the revenue contribution of individual customers and the effectiveness of sales strategies in acquiring high-value contracts.

Average Revenue Per User (ARPU): ARPU measures the average revenue generated per user over a specific period. It helps understand each user's revenue contribution and the impact of pricing strategies on overall revenue.

ARPU = Total Revenue / Number of Users

ARPU is crucial for evaluating the effectiveness of upselling and cross-selling strategies and for identifying opportunities to increase revenue per user.

Customer Acquisition Cost (CAC): CAC is the total cost of acquiring a new customer. It includes marketing, sales, and other costs associated with attracting and converting leads into paying customers.

CAC = Total Sales and Marketing Expenses / Number of New Customers Acquired

CAC is crucial for understanding the efficiency of a company’s sales and marketing efforts. A lower CAC indicates more cost-effective customer acquisition, which can positively impact profitability and valuation.

Customer Lifetime Value (LTV): LTV is the total revenue a business can expect to earn from a customer over the entire relationship duration.

LTV = ARPU × Customer Lifetime (Months or Years)

LTV helps assess the customer base's long-term value and the effectiveness of retention strategies. A higher LTV suggests that the company successfully retains customers and maximizes their value, which is a positive indicator of valuation.

LTV to CAC Ratio: The LTV to CAC ratio is a critical metric that measures the relationship between a customer's lifetime value and the cost of acquiring that customer. This ratio helps determine how effectively a company uses its resources to acquire valuable customers.

LTV to CAC Ratio = LTV / CAC

An LTV to CAC ratio of 3:1 is often considered healthy, indicating that the value generated from customers is three times the cost of acquiring them. This metric provides insight into the sustainability and efficiency of the company's growth strategies.

Churn Rate: Churn rate is the percentage of customers who cancel their subscriptions within a given period. It is a critical metric for SaaS businesses, directly impacting revenue stability and growth.

Churn Rate = Number of Customers Lost During a Period / Total Number of Customers at the Start of the Period

A lower churn rate indicates higher customer retention, contributing to predictable revenue streams and enhancing the company’s valuation.

Conversion Rate: The conversion rate measures the percentage of prospects who convert into paying customers. It is an important metric for evaluating the effectiveness of marketing and sales strategies.

Conversion Rate = Number of New Customers / Number of Leads or Trials × 100

A higher conversion rate indicates more efficient customer acquisition efforts, which can positively impact revenue growth and profitability.

Gross Margin: Gross margin represents the percentage of total revenue that exceeds the cost of goods sold (COGS). For SaaS businesses, COGS typically includes cloud infrastructure costs, customer support, and other direct costs associated with delivering the service.

Gross Margin = (Revenue − COGS) / Revenue × 100

A higher gross margin indicates better control over production costs and higher profitability, making it an important metric for assessing operational efficiency and valuation.

The Rule of 40: The Rule of 40 is a benchmark used to evaluate the balance between a SaaS company's growth and profitability. It states that a SaaS company's combined growth rate and profit margin should be at least 40%. This metric helps investors and analysts assess whether a company is growing efficiently and sustainably.

Rule of 40 = Growth Rate + Profit Margin

For example, if a company has a 25% growth rate and a 20% profit margin, its Rule of 40 score would be 45%, indicating strong performance. This metric is particularly useful for evaluating the trade-offs between growth and profitability and ensuring that a company is not sacrificing one for the other excessively.

These key metrics—MRR, ARR, ACV, ARPU, CAC, LTV, churn rate, conversion rate, gross margin, and the Rule of 40—are essential for accurately valuing a SaaS business.

They provide a comprehensive view of the company's revenue stability, customer acquisition and retention efficiency, operational profitability, and overall growth potential.

By carefully analyzing these metrics, stakeholders can gain valuable insights into the financial health and future prospects of a SaaS business, leading to more informed valuation decisions.

When it comes to valuing early-stage startups, Finro Financial Consulting offers a level of service that aligns perfectly with the unique demands of these businesses. Here’s what makes Finro the ideal choice:

Finro tailors its valuation services to fit the distinct needs of each startup. Rather than using a generic approach, we'd like to go into your specific business model, growth potential, and industry details. This personalized method ensures that our valuations truly reflect the unique aspects of your business, providing a more accurate and meaningful assessment.

In the fast-paced startup environment, timing is crucial. Finro is dedicated to delivering efficient and swift valuations, allowing you to move forward with important negotiations and strategic decisions without unnecessary delays. We understand that every moment counts, and our team is committed to providing timely results without compromising on quality.

Startups are inherently dynamic, with needs that can change rapidly. Finro’s flexible approach allows us to adapt our processes to meet your evolving requirements. This adaptability ensures that we can meet your needs as they change, offering a level of service that remains relevant and responsive throughout your growth journey.

Personalized attention is a cornerstone of Finro’s service. Unlike larger firms where you might feel like just another client, at Finro, you receive dedicated support from a consultant who is deeply familiar with your business. This ensures better communication, insightful valuations, and a smoother overall experience.

Finro offers cost-effective valuation solutions that do not compromise on quality. Our competitive and transparent pricing ensures you receive top-tier services without the exorbitant costs often associated with big-4 firms. This approach allows you to allocate more resources towards growing your business while obtaining high-quality valuations.

In summary, Finro Financial Consulting is not just another valuation firm; we are a partner dedicated to understanding and supporting your startup’s journey. Our personalized, efficient, and cost-effective services are specifically designed to meet the unique needs of early-stage businesses, providing you with the insights and support you need to succeed.

Valuing a SaaS business is a complex yet essential task that requires a deep understanding of the company's financial and operational metrics. From the early stages of an idea to the more mature phases of Series C and beyond, the appropriate valuation methods evolve to reflect the growing stability and financial data available.

We explored various valuation methods such as the Revenue Multiple, EBITDA Multiple, and Discounted Cash Flow (DCF) approaches, each offering unique insights and catering to different stages of a startup's lifecycle. Understanding key SaaS metrics like MRR, ARR, ACV, ARPU, CAC, LTV, churn rate, conversion rate, and gross margin is crucial for developing accurate valuations that attract investors and guide strategic decisions.

Choosing the right valuation partner is equally important. Finro Financial Consulting stands out by providing tailored, efficient, cost-effective services specifically designed for early-stage startups. With a deep commitment to understanding your business's unique aspects, Finro delivers valuations that are not only accurate but also insightful and aligned with your growth trajectory.

In the fast-paced and dynamic world of startups, having a reliable and knowledgeable valuation consultant like Finro can make a significant difference. By choosing Finro, you are not just getting a valuation; you are gaining a dedicated partner invested in your success and committed to helping you navigate the challenges and opportunities ahead.

As your startup continues to grow and evolve, the insights and support from a trusted valuation partner will be invaluable. Finro's expertise and personalized approach ensure that you are well-equipped to make informed decisions, attract the right investors, and achieve your business goals.

Tailored Methods: Use Revenue Multiple, EBITDA, and DCF for SaaS valuation.

Essential Metrics: Track MRR, ARR, ACV, ARPU, CAC, LTV, churn, conversion, gross margin.

Stage-Specific Approaches: Apply different methods for various startup stages.

Finro's Service: Personalized, efficient, cost-effective valuations.

Investor Attraction: Accurate valuations aid strategic decisions and investor interest.

A good LTV to CAC ratio for a SaaS company is often considered to be 3:1. This means that the lifetime value of a customer should be three times the cost of acquiring that customer. This ratio indicates that the company is efficiently generating value from its customers relative to the cost of acquiring them.

The Rule of 40 is a benchmark used to evaluate the balance between a SaaS company's growth rate and profitability. It states that a SaaS company's combined growth rate and profit margin should be at least 40%. For example, if a company has a 25% growth rate and a 20% profit margin, its Rule of 40 score would be 45%, indicating strong performance.

To value a SaaS business, you can use several methods:

Revenue Multiple: This involves applying a multiple to your annual or monthly recurring revenue (ARR or MRR) to estimate enterprise value.

EBITDA Multiple: If the company is EBITDA positive, you can use an EBITDA multiple to value the business.

Discounted Cash Flow (DCF): This method involves projecting future cash flows and discounting them back to their present value using an appropriate discount rate.

Key Metrics: Analyzing metrics such as MRR, ARR, ACV, ARPU, CAC, LTV, churn rate, conversion rate, gross margin, and the Rule of 40 can provide a comprehensive view of the company's financial health and growth potential.

Item descriptionValuing a SaaS startup involves several steps and considerations:

Early Stages (Idea to Pre-Seed): Often, startups in these stages do not need a formal valuation and can use unpriced rounds (SAFE or convertible notes) to raise funds.

Pre-Seed and Seed Stages: Valuations may use qualitative methods (e.g., Berkus Method, Risk Factor Summation Method) or quantitative methods (e.g., Venture Capital Method, Comparables Method).

Series A and B: Startups at this stage may use the Comparables Method, focusing on revenue multiples and potentially EBITDA multiples if they are EBITDA positive.

Late Stages (Series C and Beyond): Mature startups may use a combination of Comparables, Discounted Cash Flow (DCF), and Net Asset Value (NAV) methods to achieve a more accurate valuation. Analyzing key metrics like MRR, ARR, CAC, LTV, churn rate, conversion rate, gross margin, and the Rule of 40 is also crucial for these valuations.