AI Agents Valuation Multiples: 2025 Insights & Trends

Founder of Finro Financial Consulting. Personally leads every valuation, modeling, and M&A advisory engagement.

View Lior's profile →Startup valuation, financial modeling, and M&A advisory for AI, fintech, and SaaS companies. Serving funded tech startups from pre-seed through pre-IPO.

About Finro →AI agents are no longer just a futuristic concept, they’re being used today to write code, manage workflows, generate content, and even handle support tickets with minimal human involvement.

What started as simple chatbots and assistants has evolved into autonomous tools capable of making decisions, taking action, and learning from context. And with that shift, investors, founders, and operators are starting to ask: how do we actually value these companies?

The rise of AI agents has introduced a new category that doesn’t fit neatly into existing frameworks like SaaS or traditional AI software.

Some agents act like employees. Others look more like infrastructure. As a result, the benchmarks, metrics, and expectations are still taking shape.

This article breaks down how to think about AI agent valuation in 2025, what’s included, what’s not, and where the market is headed.

We’ll also look at the key niches driving the category, the most common valuation methods, and what’s moving multiples across different use cases.

TL;DR

Topics covered in this article

- What Are AI Agents? Industry Overview & Definitions

- What Counts as an AI Agent, And What Doesn’t

- The Main Use Cases for AI Agents

- Understanding AI Agent Valuation

- Why AI Agent Valuations Are Different?

- The Challenges of Valuing AI Agents

- Key Valuation Methods for AI Agent Companies

- AI Agent Market Breakdown: Niches & 2025 Multiples

- What’s Driving AI Agent Valuation in 2025?

- Download the Full 2025 AI Agent Valuation Dataset

- Conclusion

- Key Takeaways

- Answers to The Most Asked Questions

What Are AI Agents? Industry Overview & Definitions

AI agents aren’t just another interface for GPT. They’re designed to go beyond answering questions, they take action.

Whether it’s writing code, updating a CRM, processing invoices, or summarizing meetings, these tools are built to operate semi-independently, following instructions, reasoning through context, and completing multi-step tasks without constant user input.

Unlike generic AI apps that respond to a prompt and stop, AI agents are goal-oriented. You give them an objective, and they figure out how to get it done, sometimes by calling APIs, using tools, or collaborating with other agents.

That’s a key distinction. They’re not just predictive models behind a chat window; they’re built to perform.

This shift started with tools like AutoGPT and BabyAGI that showed it was possible to chain prompts and actions together.

From there, we saw a wave of developers and startups building more specialized agents for tasks like coding, lead generation, recruiting, and legal review.

Most of them don’t market themselves as “agents”, but under the hood, that’s what they are: task-executing software with AI at the core.

So why is this category taking off now?

Three reasons:

LLM reliability is improving just enough to handle real-world use cases.

The infrastructure for chaining and tool use (LangChain, CrewAI, OpenDevin, etc.) has matured fast.

Businesses are under pressure to automate work, and agents offer a plug-and-play solution with no need to redesign entire systems.

The result is a market full of tools that look lightweight but can quietly replace hours of manual work. And that’s what’s making investors and operators pay attention.

Next, let’s take a closer look at what’s actually included in the AI agent category, and where we draw the line.

What Counts as an AI Agent, And What Doesn’t

As the term “AI agent” picks up momentum, it’s important to set a clear boundary around what actually qualifies, and what doesn’t. Just because a tool uses an LLM or calls itself “autonomous” doesn’t mean it operates like a true agent. This section breaks down how we’ve defined the category for this analysis.

✅ What’s Included

AI agents are designed to go beyond prediction and conversation. They execute. A product qualifies as an agent if it can take a high-level goal, something like “clean up my calendar,” “refactor this code,” or “pull key insights from last quarter’s data”, and figure out how to get it done with minimal input.

Most agents don’t rely on a single-step response. Instead, they break the goal into smaller tasks, make decisions based on context, and loop through reasoning until they reach an outcome.

Crucially, they also have access to tools, meaning they can call APIs, browse the web, send emails, write code, or interact with other systems to carry out their work.

What makes an AI agent feel agent-like is its ability to operate semi-independently.

It might check in occasionally (“Should I email this now or wait until Monday?”), but it doesn’t need to be prompted for every move. That’s the key difference. It works more like a junior team member than a smart search bar.

For this reason, tools like Cursor, Devin, SpellBook, Questflow, and Julius are all included, they meet the bar for autonomy, reasoning, tool use, and end-to-end execution.

❌ What’s Not Included

On the other side, there’s a long list of AI-powered tools that are impressive, but don’t qualify as agents. That includes many familiar names.

A chat-based assistant that gives you great answers but never acts on them? Not an agent. A coding autocomplete tool that finishes your function but doesn’t run tests or deploy anything? Still not an agent.

Even many “AI copilots” fall into this gray zone, they assist, but don’t execute.

We’ve also excluded tools that rely on hardcoded workflows or simple rule logic. A Zapier flow triggered by a webhook isn’t an agent unless it’s making real decisions and adapting on the fly.

The same goes for chatbot builders or LLM wrappers that act as little more than polished interfaces for GPT.

So while products like ChatGPT, Grammarly, or traditional Zapier bots are useful, they aren’t included here, because they stop short of the autonomy, reasoning, and action-taking that defines agent behavior.

🧠 Why It Matters

Drawing a clear line between “uses AI” and “is an agent” helps make sense of the market. It’s also essential when comparing valuation benchmarks or product traction.

Not everything that calls itself an agent should be valued like one, and not every AI company is building for execution.

With that in mind, let’s look at the main use cases where real AI agents are gaining traction, and where investors are starting to focus.

The Main Use Cases for AI Agents

Now that we’ve defined what AI agents are, and what they’re not, it’s time to look at where they’re actually being used.

This category isn’t just growing, it’s diversifying.

While early agents were focused on developer tasks or simple automation, today’s landscape includes tools writing marketing copy, handling customer onboarding, reviewing legal docs, and even assisting with diagnostics in healthcare.

The common thread?

These agents are built to perform real work across functions, often with minimal handholding.

Based on our analysis of 180+ companies, here are the 10 primary use case categories driving the AI agent ecosystem in 2025:

Dev Tools & Autonomous Coding: This is where the agent movement really took off. These tools go beyond autocomplete, they can write full functions, debug code, run tests, open pull requests, and even refactor large projects. Many of them operate inside the IDE or plug directly into dev workflows. Examples: Replit, Devin, AutoGPT, Cursor.

Marketing & Content Automation: From generating product descriptions and ad copy to automating campaign workflows, marketing agents are saving time across the funnel. They’re often used by lean growth teams that want output without hiring extra headcount. Examples: Writesonic, Butternut AI, Questflow, OneAI.

Sales & Customer Ops: AI agents here focus on outbound messaging, lead scoring, customer onboarding, and basic support tasks. Some act like SDRs, others replace frontline support reps, either way, they’re helping companies scale without burning human time. Examples: Cognism, Agent.ai, Fini AI.

Data & Analytics Agents: These agents act as a layer between humans and data. They can query databases, build dashboards, interpret reports, and surface insights, all using natural language. They’re especially popular with operations and product teams who want answers without writing SQL. Examples: LangChain, AskYourDatabase, Graphlit.

Healthcare & Life Sciences: In healthcare, AI agents are being used to assist with diagnostics, medical imaging, triage, and even patient engagement. While regulation adds complexity, the opportunity is massive, especially in clinical decision support and data-heavy use cases. Examples: Hippocratic AI, Codametrix, Julius.

Finance & FinOps Agents: These agents help with everything from financial planning and accounting to tax optimization, expense tracking, and forecasting. Many of them integrate with existing systems and use AI to make sense of messy financial data or recommend actions. Examples: JustPaid, Basis, Taxy, Finny.

Legal & Compliance Agents: Built for law firms, GRC teams, and legal ops, these agents review contracts, flag risks, extract clauses, or draft documents. The best ones aren’t just trained on legal language, they’re designed to mimic the reasoning lawyers bring to review. Examples: SpellBook, DeepJudge AI, TrueLaw.

Productivity & Internal Tools: These agents help teams automate notes, meetings, workflows, and project management tasks. Think of them as AI coworkers handling the stuff that eats up time but doesn’t require creative judgment. Examples: ClickUp Brain, Bardeen, Jarvis.

HR & People Ops: From resume screening to interview scheduling and onboarding, these agents streamline the people side of the business. While still early, we’re starting to see traction in hiring automation and employee support bots. Examples: Olivia, ForteAI.

PropTech & Real Asset Ops: This emerging group of agents focuses on real estate, construction, and infrastructure. They help manage leases, automate inspections, or extract data from large asset portfolios. As physical industries become more digitized, agent adoption here is picking up. Examples: OpenAgent, Beam, Alice.

This breakdown shows just how far AI agents have spread, and how different their use cases can look, even if they rely on similar tech under the hood.

In the next section, we’ll shift focus to valuation: what makes AI agent companies different when it comes to pricing, benchmarking, and growth expectations.

Understanding AI Agent Valuation

So far, we’ve defined what qualifies as an AI agent, outlined where they’re actually gaining traction, and mapped out how the market breaks down by use case.

But understanding what these companies do is only half the story.

The other half, especially for founders, operators, and investors, is figuring out how they’re being valued.

And here, things don’t follow the usual playbook.

From “Feature” to “Platform”

One of the biggest shifts we’re seeing is the transition from agent-as-a-feature to agent-as-a-platform. Early entrants in this space looked like tools, they helped you write code faster, summarize customer tickets, or automate calendar cleanup. But most were single-function wrappers built on top of GPT. Easy to launch. Easier to clone.

That’s changing fast. The next wave of agents aren’t just performing tasks, they’re sequencing actions, integrating into workflows, adapting in real-time, and in some cases, handing off decisions to other agents. They’re starting to behave more like operating systems than features.

This matters because once investors see a platform play, something sticky, extensible, and integrated, the valuation lens widens. Multiples don’t just reflect revenue. They reflect surface area.

Investor Appetite After the 2024 Hype Cycle

If 2023 was about excitement, 2024 brought the correction. The buzz around AI agents created a flood of demos, prototypes, and half-baked products. Investors took meetings. Lots of them. And then paused.

Now, post-hype, the signal is clearer: investor interest hasn’t vanished, it’s just moved downstream. What’s getting attention in 2025 are agent companies with:

Clear use cases tied to pain points

Reliable infrastructure that works beyond a demo

Workflow integration (not just UI polish)

Repeatable use that shows up in retention curves

There’s also more emphasis on business function. Coding, finance, legal, and healthcare have emerged as categories where agents can show ROI early, and investors are following that traction.

Why Metrics Differ from SaaS or Traditional AI

Valuing an AI agent company doesn’t follow the same rules as a traditional SaaS business, and it definitely doesn’t look like infrastructure AI.

Where SaaS investors are trained to look for recurring revenue and steady logins, agent-based products often show:

Bursty usage tied to specific workflows or outcomes

Variable cost structures, especially if agents use tools like browsers, APIs, or GPUs

Later-stage monetization, especially for open-source or bottoms-up plays

That said, when agent usage lands, it tends to replace a full-time role, not just shave off minutes. That creates a much stronger ROI story. The trick is getting there with enough product stability and user trust.

In the next section, we’ll walk through the main valuation methods used for agent companies, including where standard SaaS multiples break down, and where alternative benchmarks matter more.

Why AI Agent Valuations Are Different?

By now, we’ve looked at what defines an AI agent, how they’re used across industries, and how valuation potential rises with product maturity. But even with that context, it’s clear that AI agent companies don’t fit neatly into existing valuation playbooks.

Their structure, scope, and growth paths raise questions that don’t always apply to SaaS, infrastructure, or even vertical AI startups.

Here’s why they stand apart.

1. Multi-Modal, Cross-Functional by Design

Traditional AI tools tend to focus on one format (text, code, images) or one job function (e.g., customer support or sales enablement).

AI agents break that mold. The same agent might write code, use a browser, summarize data, and schedule a meeting, all within a single flow.

This multi-modal, cross-functional nature makes them harder to box in. It also makes comparisons tricky. Is it a dev tool?

A productivity platform? A vertical solution? Often it’s all three, depending on the workflow.

From a valuation standpoint, this opens the door to broader market narratives, but it also means fewer comps, more uncertainty, and a stronger need for investors to understand what the agent actually replaces.

2. Blurred Lines Between Horizontal and Vertical AI

One of the most confusing things about valuing AI agents is that many start horizontal and go vertical later, or vice versa.

You might begin with a general-purpose automation layer, and then get traction with a specific use case (say, accounting workflows or legal compliance). Or you might build a vertical agent for healthcare, but realize your architecture is generalizable.

This fluidity creates tension for investors and acquirers:

Does this company have platform potential, or is it solving one niche problem really well?

Should valuation be based on TAM expansion, or on depth of usage within a category?

Unlike traditional vertical SaaS (which grows land-and-expand), AI agents often grow by bending use cases, not stacking logos.

3. High Potential, Low Predictability

There’s no doubt that AI agents unlock huge upside. When they work, they don’t just improve productivity, they replace expensive, repeatable work. But getting there is messy.

Agents are unpredictable by nature. They might hallucinate. They might fail silently. They might work well for one customer, and break for another. And even if they’re reliable, users don’t always know how to trust them yet.

This creates a gap between the theoretical value and what early revenue shows on paper. Some investors lean in, betting on future upside. Others want proof that a workflow is sticky, repeatable, and monetizable.

The result? Valuations in the AI agent space swing wildly, not just based on metrics, but based on how believable the agent’s long-term vision really is.

In the next section, we’ll look at how these differences show up in valuation methods, including which benchmarks make sense, and which ones don’t.

| Attribute / Question | SaaS | Vertical AI | AI Agents |

|---|---|---|---|

| Target User or Function | Single team or business unit | One specific industry or use case | Cross-functional; spans roles or teams |

| Output Type | Dashboards, notifications, reports | Domain-specific answers or predictions | Multi-step actions: code, content, scheduling, etc. |

| Adoption Model | Seat-based, gradual expansion | Proof-of-value in focused workflow | Use case-driven; usage may spike then dip |

| Growth Pattern | Add logos and users | Expand within niche vertical | Penetrate workflows and automate across tools |

| Primary Valuation Driver | ARR, retention, CAC:LTV | Market size, traction, partnerships | Depth of automation, defensibility, workflow value |

| Tech Complexity | Moderate (CRUD apps, integrations) | High (data science, vertical models) | Very high (tool use, memory, planning, autonomy) |

| Market Perception | Familiar, well-benchmarked | Niche but established | New category, unclear comparables |

| Competitive Moat | Data, integrations, switching costs | Domain expertise, proprietary data/models | Execution, agent frameworks, speed of iteration |

| Comparable Companies | Many | Some | Few to none |

The Challenges of Valuing AI Agents

By this point, we’ve covered what sets AI agents apart, how their valuation trajectory differs from SaaS and vertical AI, and why traditional benchmarks often fall short. But even with the right lens, valuing these companies isn’t straightforward.

Between technical complexity, early-stage ambiguity, and fast-moving hype cycles, agent startups raise a very specific set of questions.

Let’s break down the core challenges.

1. Pre-Revenue vs. Early Traction vs. Scale

Most AI agent startups aren’t following the clean, metric-driven growth arcs that SaaS investors are used to. Some raise large rounds pre-revenue based on technical promise. Others show quick usage spikes with no clear monetization model. And a few outliers scale quickly, but often in unpredictable ways.

So what gets valued?

At pre-revenue, it’s usually team + tech + vision.

With early traction, it’s about proving repeatable usage or early GTM motion.

At scale, metrics start to matter, but even then, they don’t always map neatly to ARR multiples.

This makes the landscape uneven: two companies with similar usage can have dramatically different valuations depending on perceived defensibility, talent, or hype.

2. Market Ambiguity & Model Dependencies

Another major challenge is figuring out what market an agent company is actually in. Some pitch as workflow automation, others as dev tools, others as AI assistants, but the tech often overlaps. That market ambiguity makes it harder to compare to public comps or benchmark against peers.

And then there’s the issue of model dependency.

Are they just calling OpenAI’s API under the hood?

Do they fine-tune or build their own infrastructure?

How portable is the product if the LLM ecosystem shifts?

Investors are increasingly sensitive to this. Companies that build true abstraction layers, tool orchestration, or agentic memory systems tend to command higher valuations than those seen as UI on top of someone else’s model.

3. Technical Moat vs. LLM Wrapper

This might be the single biggest credibility filter in AI agent investing:

Is there a real technical moat, or is this just a polished wrapper?

An agent that looks great in a demo may fall apart in production. Real-world use cases often involve tool use, chaining, conditional logic, error handling, and persistence, and that’s hard to fake. Companies that invest in memory, reasoning, and reliability are slowly separating from those that just hook into OpenAI and ship a prompt.

From a valuation perspective, investors are learning to ask tougher questions:

What’s proprietary here?

What happens if GPT-5 launches tomorrow?

Can this company operate across LLM providers?

The stronger the answers, the stronger the multiple.

In the next section, we’ll dive into how these challenges shape the way AI agent startups are actually being valued, and where traditional valuation methods still hold up (and where they don’t).

Key Valuation Methods for AI Agent Companies

Now that we’ve unpacked why AI agents are tricky to value — from model dependency to market ambiguity — the next question is: how do you actually approach valuation in this space?

The short answer: you still use familiar methods, but you apply them with context.

Agent startups don’t operate like traditional SaaS, and they don’t grow like vertical AI either. That’s why it’s critical to adapt the framework to the agent’s maturity, defensibility, and actual business model — not just apply a generic multiple.

Here’s how investors and operators are thinking about it:

1. Revenue Multiple: Still the Default, But With a Big Asterisk

For AI agents with early traction or real ARR, revenue multiples are still the most common benchmark. But unlike in SaaS, you can’t just plug in the latest median from a PitchBook chart and move on.

If it’s a wrapper product with some usage but weak defensibility, the multiple is often lower than SaaS — sometimes 3–5x.

If it’s a workflow-native agent that replaces headcount and has high retention, the multiple may trend higher than SaaS — 10x+ isn’t unheard of for the right kind of traction.

What matters most is not just the number, but how believable that revenue is at scale.

2. EBITDA Multiple: Rare, But Not Irrelevant

Most AI agent companies aren’t profitable, and that’s expected. But if you’re looking at later-stage players with more enterprise customers, EBITDA becomes a credibility signal — especially in a market where burn is under more scrutiny.

That said, valuation based on EBITDA is more likely to show up in:

Private equity interest

Late-stage rounds

M&A conversations, if/when they happen

But for early-stage agent startups? You won’t hear “EBITDA” in a pitch deck — and that’s fine.

3. Discounted Cash Flow (DCF): Useful for Thoughtful Operators

DCF isn’t often used as the primary method in early-stage tech, and AI agents are no exception. But for operators, especially those with real unit economics or infrastructure-style margins, DCF can be a useful internal tool.

If you’re building something that looks more like an AI-native platform than a point solution, DCF helps frame long-term upside.

It also helps anchor investor expectations in cash potential, not just growth narratives.

Just don’t expect VCs to lead with it — but having it in your back pocket can signal financial discipline.

What About Multiples Based on Usage?

This comes up a lot with AI agents, especially those that are pre-revenue but seeing strong engagement (e.g. dev tools, automation agents, etc). Some investors use usage-adjusted benchmarks like:

Active sessions per month

Tasks completed per user

Revenue per 1,000 interactions (in freemium models)

They’re messy, and not standardized, but they give a directional sense of value when revenue hasn’t caught up yet.

In the next section, we’ll look at how these methods apply to real companies — by niche — and where 2025 multiples are trending. Spoiler: agent-first infrastructure is getting the highest premium.

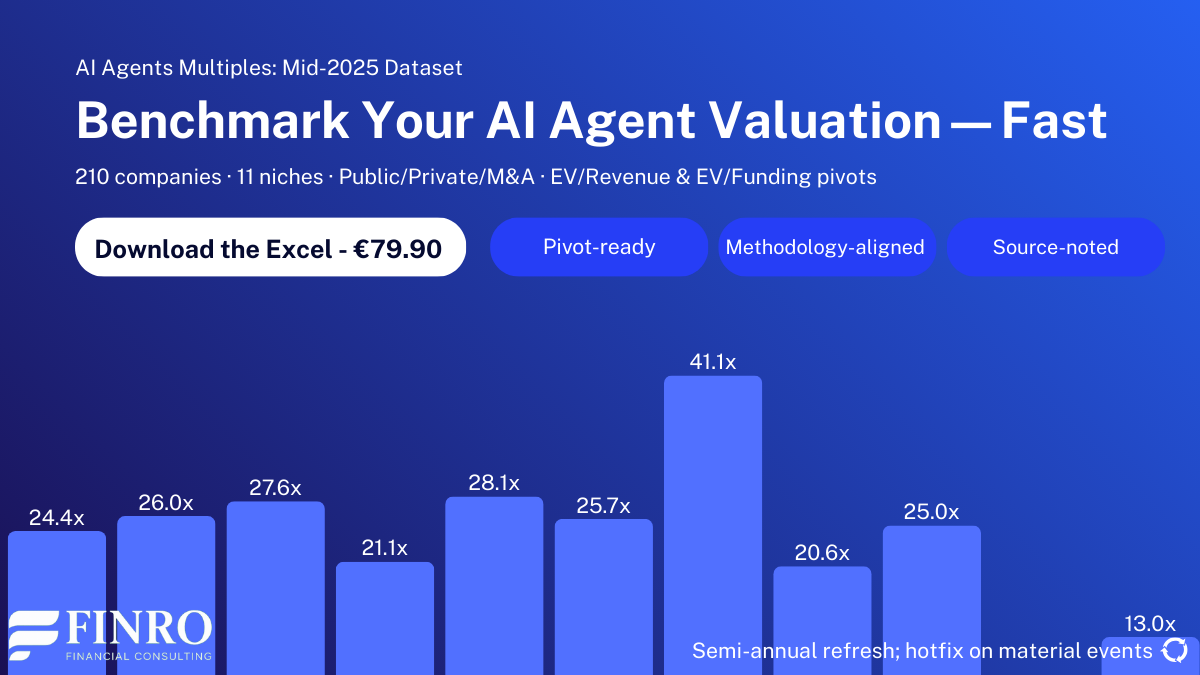

AI Agent Market Breakdown: Niches & 2025 Multiples

AI agents aren’t a single market. They span across developer tools, marketing automation, healthcare, finance, productivity software, and more. While they often get lumped together under the “autonomous agents” umbrella, each niche has its own business model, user behavior, and growth trajectory.

The dataset includes over 180 private AI agent companies, mapped across ten distinct use cases. The analysis reveals sharp differences in how investors are valuing companies, shaped by technical complexity, defensibility, revenue visibility, and integration depth.

Understanding these variations is key for anyone benchmarking AI agent startups in 2025, whether you’re raising, investing, or just trying to figure out what a reasonable multiple actually looks like.

Below is a breakdown of the main agent categories and how their valuation profiles compare.

Dev Tools & Autonomous Coding

The breakout category with the highest multiples.

This is where the most excitement and capital, is concentrated. These companies are deeply integrated into developer workflows, from AI code reviewers to full-stack agents like Devin. Many monetize early with usage-based pricing or team plans, and have strong product-led growth loops.

Their valuation multiples reflect this: ~63x average revenue multiple, the highest across all agent categories.

Valuation Drivers:

Strong technical defensibility and early infra-like behavior

High developer engagement and bottom-up adoption

Clear ROI in automating repetitive dev tasks

Finance & FinOps Agents

Fast-moving category with high willingness to pay.

These agents help automate budgeting, accounting, forecasting, and reporting. Many operate in B2B environments with high switching costs and integrations into ERP or finance systems. Valuations here are lifted by buyer urgency and the complexity of workflows.

Valuation Drivers:

Recurring revenue from automation of essential workflows

Sticky integrations with real financial systems

High trust bar = high defensibility if achieved

Legal & Compliance Agents

Complex problems, clear value if solved.

This is a niche where agents can save hundreds of hours, but only if they work reliably. From contract parsing to compliance checks, these tools aim to augment or even replace legal review processes. Valuations are strong in cases where the agent goes beyond summarization to actual decision support.

Valuation Drivers:

Domain expertise and workflow-specific knowledge

Regulatory context baked into the agent logic

High-value buyer segments with long sales cycles

Data & Analytics Agents

From dashboards to intelligent querying.

This segment includes agents that turn business data into action: querying databases, building dashboards, or generating insights. Some act as copilots for data teams; others aim to replace them entirely. Valuation multiples vary depending on product depth and adoption.

Valuation Drivers:

Usage-based models (per query or user)

Integration with data warehouses / BI tools

Ability to generate real insights, not just summaries

Marketing & Content Automation

Crowded, but still growing.

AI agents in this space help marketers generate content, write copy, run campaigns, and optimize workflows. It’s a hot category, but one that’s often criticized for low defensibility. Still, the top players, especially those with data or automation depth, command solid valuations.

Valuation Drivers:

Breadth of supported tasks

Campaign-level autonomy (vs. just writing)

B2B SaaS-style go-to-market motion

Productivity & Internal Tools

Horizontal agents for day-to-day work.

This group includes general-purpose copilots, workplace automators, and agents that help teams manage docs, meetings, or tasks. Adoption can be fast, but long-term retention is often the challenge. Valuations reflect that tension, upside exists, but stickiness is everything.

Valuation Drivers:

Embedded into core workflows (e.g. CRM, email, docs)

Enterprise expansion potential

AI-as-a-feature vs. AI-as-the-core-product

Healthcare & Life Sciences

Specialized agents with deep domain hurdles.

Healthcare-focused agents are emerging across diagnostics, clinical operations, and medical research. But because of regulation and risk, adoption is slower and more fragmented. Valuation multiples tend to trail the tech-heavy categories, unless the agent is deeply integrated into clinical systems.

Valuation Drivers:

Regulatory pathway and compliance readiness

Workflow depth (e.g., radiology, RCM, pharma)

Strategic partnerships with hospitals or payers

HR & People Ops

Emerging category still finding product-market fit.

These agents support hiring, onboarding, performance reviews, and internal communications. They’re useful but often seen as nice-to-have rather than critical. Their valuations are generally more conservative unless paired with deep automation or integrations.

Valuation Drivers:

Automation of manual HR work

Integration with HRIS or payroll systems

Expansion potential across roles or departments

PropTech & Real Asset Ops

Low competition, but early.

Agent startups in property management, construction, and asset maintenance are still rare, but the few that exist are showing promise. Valuation depends on how well the agent plugs into operational workflows and reduces manual work in real estate-heavy businesses.

Valuation Drivers:

Workflow depth in an underserved market

Domain-specific automation (leases, repairs, inspections)

Ability to generalize across asset classes

Key Takeaway:

Even within the AI agents world, valuation is not a fixed formula. It depends on who the agent serves, how defensible the tech is, and whether the use case generates recurring, reliable value. That’s why we’re seeing such a widespread in revenue multiples, from high-flying dev tools to slower-moving healthcare automation.

In the next section, we’ll examine what’s shaping those valuation differences and what investors are really looking for in 2025.

What’s Driving AI Agent Valuation in 2025?

By now we’ve seen how varied the AI agent landscape really is — from deeply vertical tools to general-purpose platforms. But beyond the numbers, what’s actually pushing valuations up in 2025?

Several recurring themes are showing up in investor conversations, pitch decks, and funding patterns. It’s no longer enough to build something clever on top of GPT — the bar has moved.

Developer Traction Still Signals Strong Potential

Whether it’s GitHub stars, DevPost hackathon buzz, or third-party APIs calling your endpoints — developer traction is a growing proxy for early PMF in technical products. Investors see active usage from builders and automation engineers as early signs of real utility, especially for developer-facing agents and open agent frameworks.

Many of the highest-valued agent companies today gained early attention from the dev community and quickly turned that into ecosystems, plugin marketplaces, or open-source adoption.

B2B Adoption Is Where the Scale Happens

There’s growing investor preference for agents with actual business adoption. Not just individual productivity tools, but agents that have made it into enterprise workflows: legal review, financial forecasting, healthcare support, etc.

The more vertical the use case — and the more critical the workflow — the more defensible the business tends to be. That’s why AI agents that specialize in B2B pain points, compliance-heavy industries, or decision-making support tend to fetch stronger multiples.

Moving Past OpenAI Wrappers

2023 and early 2024 were saturated with wrapper startups. Some raised on the back of clever UX or narrow feature sets. But now, valuations tend to favor agents that show infrastructure independence, multi-model compatibility, or more advanced agentic behavior.

In short, if OpenAI changes something tomorrow and your entire roadmap breaks — investors are assigning a lower ceiling. If your agent can plug into Claude, Mistral, or even local LLMs and keep humming? Much more interesting.

Workflow Defense Is the New Moat

Forget the UI — the real moat is whether your agent owns a workflow.

Can it orchestrate other tools? Is it embedded deep in team operations? Is switching to another agent inconvenient?

This is where we see the emergence of agent-native ecosystems, where agents aren’t just features — they’re becoming the default interface for tasks. Companies building this kind of stickiness are commanding valuations that look more like platforms than tools.

Download the Full 2025 AI Agent Valuation Dataset

This article breaks down the trends shaping the AI agent market — but the real value lies in the data behind it.

We’ve compiled a structured dataset covering 180+ private AI agent companies, grouped into 10 core use cases, and enriched with both high-level market insights and company-level details.

Whether you’re analyzing the space, benchmarking a startup, or advising a client — this dataset gives you the clarity most people miss.

What You’ll Get

Full company-level data for 180+ AI agent startups, including:

Company name and description

Functional category (e.g. dev tools, marketing, healthcare)

Estimated valuation

Total capital raised

Average revenue multiple (when available)

Summary analysis by category, including:

Total number of companies per use case

Average valuation and funding per category

Average revenue multiple

Total revenue and capital raised by segment

Format & Use

Delivered as a clean, structured Excel spreadsheet — ready for analysis, filtering, or presentation use. Built for founders, analysts, investors, and operators who want an edge in one of the most dynamic corners of AI.

Price: €39.90

→ Instant access. One file. No fluff. No subscription.

Conclusion

AI agents are no longer a fringe category — they’ve become a serious slice of the early-stage tech market, with capital flowing into everything from autonomous dev tools to vertical workflow automation.

But as this space grows, so does the complexity of evaluating it.

Valuations are no longer driven just by flashy demos or OpenAI integrations. In 2025, the real drivers are category maturity, workflow defensibility, cross-model independence, and early traction with developers or enterprise users.

If you’re an investor, founder, or operator working in or around this space, understanding these nuances isn’t optional — it’s essential.

And while no chart or spreadsheet can predict the future, a grounded view of where the money is flowing, how valuations cluster, and which niches are over- or under-valued can give you an edge.

The dataset we’ve compiled is designed to give you exactly that.

Thanks for reading.

Key Takeaways

1. AI Agent Valuations Vary Widely: Valuations depend heavily on niche, defensibility, and traction — not just technical capabilities or model integrations.

2. Dev Tools Dominate Capital Flow: Developer-focused agents lead in funding and volume, but other verticals show stronger average valuations per company.

3. Workflow Ownership Drives Premiums: Agents embedded in real workflows with switching costs attract higher valuations than standalone tools or wrappers.

4. Investors Want More Than GPT Wrappers: Valuable agents show multi-model support, automation depth, and functional independence from any single LLM provider.

5. Category Insights Beat Generic Benchmarks: Valuation multiples vary significantly by use case — benchmarking only works if you know the specific market you’re comparing to.

Answers to The Most Asked Questions

-

An AI agent is an autonomous or semi-autonomous system that can perform tasks, make decisions, and act on behalf of users or organizations.

-

Valuing AI agents depends on traction, defensibility, use case, and revenue potential — not just technical capabilities or model integrations.

-

Key categories include dev tools, productivity agents, marketing automation, customer ops, healthcare, legal, finance, HR tech, and proptech agents.

-

Not always. The most valuable agents offer multi-model support, orchestration, workflow ownership, and defensibility beyond ChatGPT-based interactions.

-

Developer tools and productivity agents lead in capital raised, but legal, healthcare, and B2B-focused agents often show higher average valuations per company.

AI Startup Valuations in 2025: Benchmarks Across 400+ Companies