Aeron Sullivan

Founder and CEO, Pangea.io

By Lior Ronen | Founder, Finro Financial Consulting

The financial sector, once known for its inefficiencies and complexities, has undergone a revolutionary transformation with the rise of fintech startups.

These companies have disrupted traditional financial services, introducing innovative solutions across various domains such as payments, lending, wealth management, and insurance.

As the fintech landscape continues to evolve rapidly, driven by advancements in technology and shifting consumer expectations, understanding how to accurately value these startups has never been more critical.

In this article, we explore the comprehensive methods, factors, and metrics necessary for valuing fintech startups. We delve into the key pillars of fintech, compare the valuation of fintech companies versus traditional financial institutions, and introduce the latest trends shaping the industry in 2024.

By examining these trends—such as AI and machine learning, decentralized finance (DeFi), open banking, regulatory technology (RegTech), and sustainable fintech—we provide a detailed framework to help investors and entrepreneurs navigate the dynamic fintech ecosystem.

As fintech startups continue developing innovative solutions, investors have become increasingly interested in these companies.

Estimating the value of a potential investment is a crucial part of the investment process. In the case of valuing fintech companies, this process is highly challenging since they operate in rapidly evolving markets that are new territory for many investors.

In this article, we will explore how to value a fintech startup. We'll start by explaining the characteristics of successful fintech startups and why they are attractive to investors.

Then, we will discuss the different methods and metrics used to value fintech startups, including discounted cash flow, comparable company analysis, and venture capital methods.

The fintech industry is one of the most dynamic sectors in the global economy, constantly evolving as new technologies and ideas emerge. Understanding the latest trends is crucial for anyone involved in valuing fintech startups, as these developments directly impact how these companies operate, grow, and compete.

In this section, we’ll explore the most significant trends currently shaping the fintech landscape. These trends not only influence the strategic direction of fintech companies but also play a pivotal role in how they are assessed and valued in the market.

By examining these trends, we can gain deeper insights into the factors driving innovation and disruption within the core areas of fintech, setting the stage for a more comprehensive evaluation.

The fintech landscape is rapidly evolving, with innovative technologies like artificial intelligence (AI) and machine learning at the forefront of this transformation. These technologies are being harnessed to enhance various aspects of financial services, from customer service to risk management.

For example, AI-powered robo-advisors like Betterment, valued at approximately $1.3 billion, and Wealthfront, valued at $1.4 billion, provide personalized financial advice at scale, offering tailored investment strategies based on individual user data.

Similarly, Stripe, now valued at around $50 billion, utilizes AI to enhance payment processing and fraud detection, making it one of the most valuable fintech companies globally. The integration of AI not only boosts operational efficiency but also drives customer retention, making startups that leverage these technologies particularly attractive to investors.

Consequently, AI-driven fintech companies often command higher valuations due to their scalability and the long-term growth potential they represent.

Another trend gaining momentum in the fintech world is decentralized finance, or DeFi, which leverages blockchain technology to offer financial services without the need for traditional intermediaries like banks.

DeFi platforms such as Aave, which has a market cap of approximately $900 million, and Uniswap, valued at over $1 billion, provide services such as lending, borrowing, and trading in a decentralized, transparent manner, accessible to anyone with an internet connection.

This democratization of financial services is disrupting the traditional financial ecosystem, presenting both opportunities and challenges for valuation. While the growth potential of DeFi startups is immense, their valuations must consider the inherent risks of operating in an unregulated and highly volatile environment.

Open Banking is also reshaping the fintech landscape by fostering greater collaboration between traditional financial institutions and third-party providers. By allowing secure access to customer financial data, Open Banking is spurring the development of innovative products and services that enhance customer experience and drive competition.

Leading companies in this space include Plaid, valued at around $13.4 billion, which provides a platform that connects consumer bank accounts to apps and services, and TrueLayer, recently valued at $1 billion, which offers a similar service enabling third-party applications to connect to bank data.

Startups that capitalize on Open Banking's potential can see rapid customer acquisition and retention, which in turn positively impacts their revenue projections and overall valuation.

Aeron Sullivan

Founder and CEO, Pangea.io

What can I say? Is there a better financial modeling expert for startups than Lior? I doubt it.

Lior is fast, precise, fastidious, and intuitively understands the stage startups are in and what they need in a financial model. I would hire Lior for any FP&A role any day.

I have absolute confidence if you use him for consultant services in the financial space you will not be disappointed.

The rise of Regulatory Technology, or RegTech, is another trend significantly impacting the fintech industry. As the regulatory environment becomes increasingly complex, fintech companies are turning to RegTech solutions to streamline compliance processes.

Companies like ComplyAdvantage, valued at $700 million, and Onfido, valued at around $600 million, use automation, AI, and advanced analytics to monitor transactions, ensure data protection, and reduce the cost and time associated with regulatory compliance.

Startups specializing in RegTech are particularly appealing to investors, as they offer the dual benefit of reducing regulatory risks and enhancing operational efficiency, often leading to higher valuations.

Lastly, there is a growing focus on sustainable and ethical fintech, driven by increasing consumer and investor demand for socially responsible financial products. Startups that prioritize environmental, social, and governance (ESG) factors in their operations and offerings are gaining traction.

Aspiration, for instance, which focuses on providing socially conscious banking and investing services, is valued at approximately $2.3 billion.

Similarly, Trine, a platform that allows people to invest in solar energy projects, is making waves in the sustainable fintech space. These companies are not only contributing to a more sustainable financial ecosystem but are also enhancing their brand value, which can lead to higher customer loyalty and attract ESG-focused investors. As the market for ethical financial products expands, these startups are likely to see their valuations rise in response to their alignment with these values.

| Trend | Description | Key Impact on Valuation |

|---|---|---|

| AI and Machine Learning | Enhances customer service, risk management, and efficiency. | Drives scalability, improves customer retention. |

| Decentralized Finance (DeFi) | Leverages blockchain to offer financial services without intermediaries. | High growth potential, but with regulatory and volatility risks. |

| Open Banking | Enables secure access to financial data for third-party services. | Increases customer acquisition, boosts innovation. |

| RegTech (Regulatory Technology) | Streamlines compliance processes using AI and automation. | Reduces regulatory risks, enhances operational efficiency. |

| Sustainable and Ethical Fintech | Focuses on ESG factors, appealing to socially responsible investors. | Attracts ESG |

The fintech sector is being shaped by powerful trends like AI, DeFi, Open Banking, RegTech, and sustainable finance. These trends not only influence how fintech companies operate but also play a crucial role in how they are valued. Understanding these developments is key to making informed valuation assessments.

As we move into the next section, which explores the Four Pillars of Fintech—Payments and Transactions, Lending and Financing, Wealth Management and Investment, and Insurance—it becomes evident how these trends are deeply interwoven with the core areas of fintech.

Each pillar is being transformed by these innovations, and their influence on valuation is undeniable. By grasping the latest trends, you gain a comprehensive view of the forces driving change within each of these pillars, allowing for a more nuanced and accurate valuation of fintech startups.

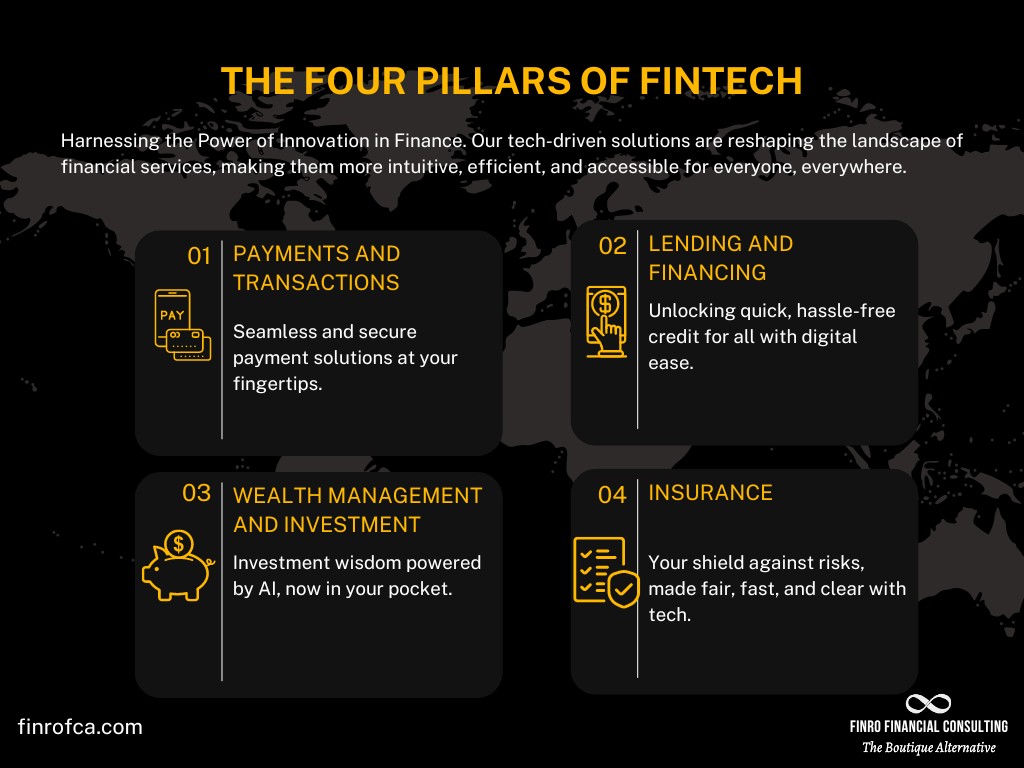

Today, the fintech industry stands on four primary pillars, each representing a core area where technology has been applied to enhance traditional financial services.

These pillars, as we'll explore, include Payments and Transactions, Lending and Financing, Wealth Management and Investment, and Insurance.

This sector of fintech encompasses all types of payment processing, including peer-to-peer payments, mobile payments, and online transactions. The goal of fintech companies in this space is to make payments more efficient, secure, and accessible.

For example, Venmo and Square Cash enable quick and easy peer-to-peer transactions, disrupting the traditional model of bank transfers. Similarly, companies like Stripe and Square provide businesses with robust platforms to accept and manage online payments, driving efficiency and reducing the complexity of managing transactions.

Cryptocurrency-based payment platforms, such as BitPay, are also gaining traction, offering an alternative way of handling online transactions.

Fintech companies have revolutionized the way loans and financing are provided to individuals and businesses. By leveraging technology, they can offer faster and more convenient access to credit than traditional financial institutions.

Platforms like LendingClub and Prosper offer peer-to-peer lending services, allowing individuals to lend to or borrow from their peers directly. OnDeck and Kabbage provide fast and convenient small business loans, streamlining the typically tedious and time-consuming loan approval process.

Moreover, fintech companies like Affirm and Klarna have changed the retail landscape by offering instant point-of-sale financing.

Fintech is making financial management and investment services accessible to everyone, not just to those with substantial wealth. This sector includes robo-advisors, online brokerages, and digital asset management.

Robo-advisors, like Betterment and Wealthfront, use algorithms to manage portfolios and offer investment advice, which dramatically lowers costs.

Online brokerages such as Robinhood have democratized investing by offering commission-free trading and user-friendly interfaces.

Companies like Acorns even enable investing with spare change, illustrating how fintech is breaking down traditional barriers to investment.

Known as Insurtech, this fintech sector is transforming the way insurance products and services are delivered.

It involves leveraging technology for policy management, claims processing, and underwriting, making insurance more affordable, accessible, and transparent.

Oscar Health, for instance, uses technology to offer a user-friendly approach to health insurance, while Lemonade uses AI and machine learning to process insurance claims instantly.

Companies like Metromile and Root provide usage-based car insurance, allowing premiums to reflect actual usage rather than estimated averages. These examples demonstrate how fintech is changing traditional insurance models.

Carving out a unique niche in the fintech landscape, Neo banks have emerged as fully digital financial institutions that challenge traditional banking norms. These innovative platforms offer banking services without the need for physical branches, reflecting the ever-evolving digital demands of modern consumers.

Notable Neo banks include Chime, Mercury, and Varo in the US and N26, Revolut, Monzo, and Bunq in Europe, each bringing unique offerings to their respective markets.

Primarily fitting within the Payments and Transactions pillar of the fintech sector, Neo banks' core offerings revolve around mobile banking, digital debit cards, and online payments.

They provide a completely digital platform, empowering customers to manage their finances anytime, anywhere, at their convenience.

What sets Neo banks apart from traditional financial institutions is their unwavering focus on the customer. They leverage technology to offer services like instant account setup, fee-less transactions, real-time spending alerts, and competitive interest rates on deposits, thus creating a compelling user experience.

However, the adaptability of Neo banks goes beyond the Payments and Transactions pillar. Many Neo banks are broadening their services, venturing into other pillars of the fintech sector such as Lending and Financing or Wealth Management and Investment.

This diversification, which may include offering personal loans or investment services, underscores their innovative drive and commitment to meeting a range of customer needs.

The influence of Neo banks, therefore, extends beyond a single pillar, highlighting their potential to transform the entire fintech industry.

| Criteria | Traditional Banks | Neo Banks |

|---|---|---|

| Platform | Physical Branches + Online/Mobile | Fully Digital (Online/Mobile) |

| Services | Broad range (Loans, Deposits, Mortgages, etc.) | Focused (Mostly Payments & Transactions) |

| Customer Interaction | In-Person and Digital | Mostly Digital |

| Setup Time | May take days with paperwork | Instant setup online |

| Fees | Higher fees for services | Lower or no fees |

| Interest Rates | Lower interest rates on deposits | Higher interest rates on deposits |

| Innovation | Slower due to legacy systems | Rapid due to advanced tech |

| Customer Experience | Traditional, often bureaucratic | Streamlined, customer-centric |

| Regulatory Compliance | Complex, more regulated | Simpler, less heavily regulated |

| Access to Services | May be restricted in some areas | Global access via internet |

Fintech startups and traditional financial institutions represent two distinct facets of the financial sector, each requiring unique valuation approaches.

Traditional financial institutions, such as banks and insurance companies, are typically valued based on their historical performance, with an emphasis on established revenue streams, stable customer bases, and adherence to a complex regulatory framework. These entities operate in a mature market where growth is often steady but incremental, and their valuation methods, such as price-to-earnings (P/E) ratios or book value, reflect this stability.

On the other hand, fintech startups are characterized by their agility, innovation, and potential for rapid growth. These companies often operate at the cutting edge of technology, introducing disruptive models that challenge the status quo in financial services.

For instance, while traditional banks rely on long-established practices for lending and payments, fintech startups may utilize decentralized finance (DeFi) platforms that remove traditional intermediaries, offering faster and more accessible services. This innovative approach can lead to higher growth potential, but also comes with increased risk and uncertainty, which must be factored into their valuation.

Moreover, fintech startups tend to emphasize customer experience and scalability, often leveraging artificial intelligence (AI) and machine learning to offer personalized services that traditional institutions may struggle to provide due to legacy systems. This customer-centric focus, combined with the ability to scale rapidly, often makes fintech startups more appealing to investors looking for high returns, despite the higher risk associated with early-stage companies.

Another key difference is in how these entities navigate regulatory environments. Traditional financial institutions are deeply embedded in a highly regulated industry, where compliance is both a significant cost and a barrier to entry. In contrast, fintech startups often turn to regulatory technology (RegTech) to streamline compliance processes, allowing them to innovate more freely and at lower costs. This ability to adapt quickly to regulatory changes can be a competitive advantage, although it also means that fintech companies must be agile in managing the regulatory risks that come with operating in a fast-evolving sector.

Additionally, the rise of open banking—a trend where banks share financial data with third-party providers—further highlights the divergence between traditional and fintech approaches. Traditional institutions might view this trend with caution, balancing it with their need for security and control, whereas fintech startups often see it as an opportunity to innovate and enhance customer engagement by offering new, integrated financial services.

Finally, the growing importance of environmental, social, and governance (ESG) factors is increasingly influencing how both fintech startups and traditional institutions are valued. While many traditional financial institutions are beginning to integrate ESG principles into their operations, fintech startups, being newer and more adaptable, often have an advantage in aligning their business models with these values, attracting socially conscious investors.

In summary, while traditional financial institutions are typically valued through established, backward-looking metrics that emphasize stability and historical performance, fintech startups require a forward-looking approach. This approach must account for their potential to disrupt markets, scale quickly, and align with emerging trends like DeFi, AI, open banking, RegTech, and sustainability. Understanding these nuances is essential for accurately assessing the value of fintech companies in today’s rapidly changing financial landscape.

| Evaluation Aspect | Fintech Startups | Traditional Financial Institutions |

|---|---|---|

| Business Model | Disruptive, technology-driven | Traditional, established |

| Growth Potential | High, based on market disruption and technology adoption | Steady, based on market trends and economic conditions |

| Operating Costs | Lower due to technology efficiencies | Higher due to physical infrastructure |

| Profitability | Potential for high profitability, but often initially unprofitable | Steady profitability based on existing customer base and diversified services |

| Regulatory Environment | Complex, but less than traditional banks | Highly regulated, with many compliance costs |

| Valuation Approach | Forward-looking, based on growth potential and market penetration | Backward-looking, based on financial performance and regulatory compliance |

| Market Share | Lower but growing | Higher due to established presence |

| Risk | High due to competitive, fast-paced environment | Moderate due to stable market position and diversified risk |

| Capital Structure | Often reliant on venture capital and fundraising rounds | Funded through customer deposits, loans, and equity issuance |

In the rapidly evolving landscape of financial services, the advent of financial technology, or fintech, has spawned a new breed of startups determined to revolutionize the industry.

These trailblazing enterprises are redefining the fabric of traditional financial services with their innovative solutions in payments, lending, wealth management, and insurance.

When it comes to gauging their value, it's not a linear path but rather a multifaceted evaluation encompassing seven key aspects that are crucial to understanding their true worth.

Appraising a fintech startup goes beyond conventional financial metrics, demanding an in-depth understanding of the complexities inherent in a highly regulated sector.

The assessment must consider regulatory constraints, compliance costs, and the intricate relationship between technology adoption and shifting consumer behaviors in a traditionally conservative financial space.

In this section, we’ll explore the seven critical aspects of fintech startup valuation, examining everything from market dynamics to financial forecasts. Each aspect is an integral part of a comprehensive appraisal, ensuring a thorough understanding of what makes these startups unique and how they stand to impact the financial services ecosystem

Aspect 1: Uniqueness

In evaluating a fintech startup, the aspect of uniqueness takes center stage.

The differentiation factor lies not merely in the sophistication of its technology but in the practical application of this technology—whether it's a groundbreaking algorithm, a user-friendly interface, or an innovative financial product—and how it uniquely addresses a market gap.

This technology's defensibility, through patents or trade secrets, is a critical component of the startup's valuation, ensuring it can sustain a competitive advantage. The startup's business model also plays a pivotal role, detailing how it will achieve financial viability. Whether it's through subscription fees, transaction fees, or a freemium model, the approach needs to demonstrate scalability and sustainability.

Additionally, understanding the startup's target demographic is essential, as their needs and behavior patterns will dictate the product's relevance and longevity in the market.

The UVP should articulate a compelling case for why customers should choose this startup over others, fulfilling unmet market needs with a clear solution. Further, the startup's strategic plans for growth are integral to its valuation.

The ability to increase market share, the presence of network effects to stimulate organic growth, and strategic partnerships all factor into the potential scale of the venture.

In sum, a fintech startup's valuation is deeply influenced by its distinctiveness in the marketplace. Investors must thoroughly examine these elements of uniqueness, from technology to target market engagement, to assess the startup's ability to flourish and transform the landscape of financial services.

This comprehensive understanding of uniqueness is fundamental to establishing a well-rounded and forward-looking valuation.

Aspect 2: Market Position

Assessing a fintech startup's market position is a critical aspect of its valuation. This evaluation encompasses identifying where the startup fits within the fintech landscape, which requires a thorough analysis of its competitive environment.

An investor needs to consider how the startup's product or service offerings measure against existing market alternatives, focusing on distinctive features, pricing, and the customer experience delivered.

Market share is a key indicator of a startup's current market penetration and provides a snapshot of its market acceptance.

Equally telling is the startup's brand strength and recognition—how well-known is the startup amongst potential customers and within the fintech community, and what is the public's perception of the brand?

Insights can be gleaned from customer feedback, media mentions, and metrics like net promoter scores, which collectively paint a picture of the brand’s reputation and its capacity to foster customer loyalty.

The degree of market saturation also informs the startup's market position. A startup operating in a market with ample room for growth faces different challenges and opportunities compared to one in a highly competitive, saturated market where differentiation becomes key to survival.

Looking forward, it's important for investors to project the startup's growth potential, considering the addressable market size, fintech adoption rates, and the startup's potential to diversify into new markets or product lines.

The startup's scalability, its adaptability to market shifts, and the ability to capitalize on new opportunities are pivotal aspects that influence its market position and, consequently, its valuation.

Understanding where the startup currently stands and its potential to grow offers a comprehensive perspective on its market position as a component of its overall valuation.

Aspect 3: Growth Potential

Growth potential is a decisive aspect of a fintech startup's valuation, reflecting its future prospects and long-term viability.

This facet of valuation necessitates a comprehensive understanding of the market size and the startup's potential to expand within it.

Estimating the market's volume and value, which hinges on user numbers and overall revenue, sets the stage for deeper analysis.

Yet, this present-day snapshot is only the starting point.

The startup's growth potential is appraised by looking ahead—forecasting how market trends, technological developments, and regulatory landscapes might bolster or restrict its expansion.

This foresight into the market's trajectory is crucial as it shapes the startup's strategic direction and influences investor expectations.

The ability to scale effectively, to increase revenue significantly while managing cost proportionately, is a testament to the startup's operational model and market strategy.

Moreover, the agility of a startup's product or service offerings—its capacity to pivot in response to evolving market requirements and technological innovation—directly correlates with its growth potential.

A startup that can adapt, refine its offerings, and capture emerging market opportunities is likely to see its value appreciably increase. Investors are on the lookout for such adaptive qualities, viewing them as indicators of a startup's ability to thrive amidst the fintech industry's rapid changes and to harness these changes for commercial gain.

The growth potential aspect, therefore, is a blend of current market understanding and predictive analysis, giving a rounded view of the startup's capacity to grow and scale.

Aspect 4: Financials

The financials are a key aspect of a fintech startup's valuation, often seen as the quantifiable backbone of the company's valuation narrative.

Investors delve beyond the surface of profit and loss statements to understand the underlying financial health and strategic direction of the company, appreciating that fintech startups may prioritize growth and market share over short-term profitability.

A rigorous analysis of the startup's revenue streams, cost structures, and cash flow is conducted to determine the robustness and scalability of its business model. This analysis aims to ascertain the viability of how the startup generates revenue—be it through one-time transactions, recurring subscriptions, or other monetization tactics—and the sustainability of these income sources.

Expenses are scrutinized for efficiency, and cash flow trends are reviewed to assess whether the startup can sustain its operations and growth with minimal external funding.

Furthermore, constructing financial projections is an integral part of understanding the startup's financial aspect of valuation. These are not arbitrary guesses but are grounded in historical financial performance, market conditions, and strategic initiatives. Projections offer a window into the future, forecasting how the startup's financials may develop with expansion and scale.

They address critical queries regarding the path to profitability, anticipated growth rates, and key financial milestones. By quantifying future potential, investors can better align the startup's projected financial trajectory with their valuation expectations and investment objectives.

Aspect 5: Team

The team behind a fintech startup is a crucial aspect of its valuation, reflecting the human capital that drives the venture's strategic and operational success.

Investors scrutinize the leadership team's quality, considering their combined expertise, industry experience, and historical performance as strong indicators of future success.

The depth of the team’s skill set in areas critical to fintech—such as technological innovation, financial acumen, and strategic business development—is meticulously evaluated to gauge the team's proficiency in steering the company through the sector's complexities.

In assessing the team, investors look for a blend of visionary leadership and practical execution ability. The founders and key executives should not only possess a clear and compelling vision for the company’s future but also show a steadfast commitment to achieving the company’s objectives. This commitment is often evidenced through past successes and the team's persistence through the startup's developmental phases.

The team's dynamic, including how well they work together and complement each other’s strengths, also plays a significant role in the startup's valuation.

Strong leadership is considered a valuable asset, as it can significantly influence a startup's ability to innovate, secure funding, enter new markets, and ultimately, achieve its business goals. The leadership team's capabilities, therefore, are not just supportive details but central to the narrative of the startup's valuation.

Aspect 6: Risks

Understanding the risk profile is a fundamental aspect of fintech startup valuation, as it shapes the perception of the startup's future performance and stability.

Investors meticulously analyze a spectrum of risks that a fintech startup might face, which can range from regulatory challenges due to stringent and ever-changing financial regulations to technological risks like cyber threats and the pace of tech obsolescence.

Furthermore, market risks are assessed to understand how economic fluctuations and changes in consumer behavior could affect the demand for the startup's services. Competitive risks also warrant a thorough evaluation, as they encompass the potential for market share erosion due to actions by current competitors or the entry of new players.

Each type of risk is weighed for its probability and potential impact on the startup’s operational continuity and financial health.

An investor’s ability to identify and comprehend these risks, combined with an assessment of the startup's strategies to mitigate them, is vital. It speaks to the company’s resilience and adaptability in the face of uncertainties.

The risk assessment not only aids in quantifying the potential threats to cash flow and growth but also informs the strategic decisions that shape the overall valuation of the fintech startup.

This multifaceted understanding of risks contributes to a well-rounded investment analysis, ensuring that decisions are made with eyes wide open to both the opportunities and the challenges inherent in the fintech sector.

Aspect 7: Valuation

The valuation of a fintech startup represents the convergence of artistry and analytics, an intricate process that harmonizes a range of valuation techniques to account for the startup's unique features and competitive environment.

This critical aspect of the valuation employs conventional methods like discounted cash flow (DCF) analysis, comparisons with similar companies, and cost-to-duplicate assessments, which lay the groundwork for a preliminary valuation figure.

Yet, given the distinct dynamics of fintech enterprises, additional specialized valuation methodologies are warranted.

These tailor-made approaches are designed to reflect the specific business models and market conditions of fintech firms, factoring in the worth of intellectual property, the rate of innovation, user base expansion, and the strength of network effects.

The ensuing discussion in the article unfolds in two further sections, which delve into these two categories of valuation methods.

The next section unpacks general valuation methods applicable to all startups, including those in fintech, providing a foundation for valuation.

Following that, we explore fintech-specific valuation methods, offering insight into the unique factors influencing valuation in the fintech sector, thus furnishing a comprehensive perspective on a startup's market value.

Valuing fintech startups requires a blend of traditional valuation techniques and innovative approaches due to their unique business models and growth trajectories.

In this section, we unpack three foundational valuation approaches – the Revenue Multiple Method, the EBITDA Method, and the Discounted Cash Flow (DCF) Method.

Each method brings its strengths and considerations to the table, from the straightforward application of revenue multiples reflecting investor sentiment through the operational profitability lens of EBITDA, to the nuanced, forward-looking perspective offered by DCF.

Understanding these methods is critical for investors, entrepreneurs, and stakeholders to establish a fair valuation of fintech ventures, whether they're at the revenue-generating stage, profitability stage, or gearing up for long-term financial projections.

| Valuation Method | Basis of Valuation | Suitability | Considerations |

|---|---|---|---|

| Revenue Multiple Method | Revenue and industry revenue multiples | Startups with significant revenue, pre-profitability | Doesn’t account for profitability, growth prospects, revenue nature |

| EBITDA Multiple Method | Operational profitability (EBITDA) | Profitable startups post-growth phase | Not applicable for startups without profits; ignores financing and accounting decisions |

| Discounted Cash Flow (DCF) | Projected future cash flows discounted to present value | Mature startups with stable, predictable cash flows | Complex; relies on assumptions about future performance and discount rate |

The Revenue Multiple Method is a comparative valuation tool that provides a simple, straightforward way to gauge a fintech startup's value.

The process involves determining a suitable revenue multiple, which is a coefficient indicating how much investors are willing to pay for each dollar of a company's revenue. This multiple is then multiplied by the startup's actual revenue to arrive at a valuation.

The revenue multiple can be derived from a variety of sources, including industry benchmarks, transactions involving similar businesses, or public companies operating in the same sector.

While this method is quite popular due to its simplicity, particularly with startups that are generating substantial revenue but are not yet profitable, it has its limitations. It doesn't take into account a company's profitability, growth prospects, or the nature of its revenue (recurring vs. one-time). Additionally, determining an appropriate multiple can be quite subjective and requires careful consideration of the specific context and comparable companies.

For a more detailed explanation on valuing startups using the Revenue Multiple Method, refer to this article.

The EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) Method provides an assessment of a company's operational profitability. By focusing on earnings derived strictly from business operations and removing the impact of financing and accounting decisions, EBITDA offers a cleaner picture of a company's operational performance.

For fintech startups that have moved beyond the initial growth phase and are generating steady profits, the EBITDA method can offer a suitable valuation approach. However, it's not applicable for those still in the red, as EBITDA is a measure of profitability.

As with the Revenue Multiple Method, selecting an appropriate EBITDA multiple can be subjective, depending on a variety of factors, including the startup's growth rate, risk profile, and the multiples used in the sale of similar companies.

For a more comprehensive overview of the EBITDA Method for startup valuation, please refer to this article.

The Discounted Cash Flow (DCF) Method is a more sophisticated valuation method that involves projecting a startup's future cash flows and discounting them back to present value using a suitable discount rate. The discount rate reflects the risk associated with the startup and the time value of money.

While the DCF Method is theoretically sound, its application can be quite complex and involves making several key assumptions about future performance and an appropriate discount rate. For fintech startups with stable and predictable cash flows, the DCF can provide a fair estimation of value.

However, for startups still in their growth phase with uncertain future cash flows, this method can yield less reliable results. Therefore, it's typically more suitable for mature startups or those with more predictable financial performance.

To learn more about valuing startups using the Discounted Cash Flow Method, check out this article.

1. Adjusted Revenue Multiple Method

The Adjusted Revenue Multiple Method tailors the conventional Revenue Multiple Method to better suit fintech startups, particularly those operating on a Software as a Service (SaaS) model.

Since many fintech companies generate recurring revenue through subscription services, this method utilizes an enterprise-value-to-recurring-revenue multiple.

This adjustment provides a more accurate valuation by recognizing the predictable and stable nature of recurring revenue streams, a characteristic highly prized by investors.

2. User or Transaction-Based Valuations

Many fintech companies operate as platform-based businesses, where the value of the company is closely tied to the number of active users or the volume of transactions processed.

User or Transaction-Based Valuations take these factors into account. For instance, a fintech firm may be valued based on metrics like the number of active users, user growth rate, or the volume/value of transactions processed through its platform.

This method often requires adjusting to account for user engagement, customer acquisition costs, and user retention rates.

3. Marketplace Valuation

Marketplace Valuation is particularly relevant for fintech companies that operate a marketplace, such as peer-to-peer lending platforms or cryptocurrency exchanges.

These platforms may be valued based on the value of transactions they facilitate rather than just their revenue. This method recognizes the role of fintech platforms as facilitators and values them for the marketplace they've built, not just the services they directly provide.

Remember, all of these valuation methods should be customized and applied considering the unique aspects of each fintech startup. Depending on the available data and nature of the business, a combination of methods might be the best approach.

It's also worth noting that these methods are not mutually exclusive and can be used in combination to arrive at a more comprehensive and balanced valuation.

Now that we've discussed the various methods for valuing a fintech startup, it's crucial to recognize that these valuations are deeply influenced by the performance indicators of the company. These Key Performance Indicators (KPIs) serve as quantifiable measures of a fintech startup's success, providing valuable insight into its growth, customer retention, profitability, and more.

In the next section, we will delve deeper into these KPIs, exploring their importance and how they can inform a fintech startup's valuation. Understanding these indicators is an essential step in applying the valuation methods effectively and accurately assessing a fintech startup's worth.

Assessing the value of a fintech startup goes beyond the traditional valuation methodologies. While revenue, EBITDA, and cash flows remain significant, they don't always provide a full picture, given the unique characteristics and rapid innovation in the fintech industry. It's here that Key Performance Indicators (KPIs) step in.

KPIs are quantifiable measures that help evaluate the success of an organization, a specific activity, or a particular project in which it engages. For fintech startups, KPIs offer insights into their growth trajectory, profitability, customer retention, operational efficiency, and risk levels. They essentially allow investors and stakeholders to 'look under the hood' of these startups and make informed decisions.

In this section, we'll explore some of the most pertinent KPIs that investors examine when valuing fintech startups. These range from universally applicable indicators, such as customer acquisition cost and burn rate, to fintech-specific metrics like net interest margin, prepayment rate, and default rate. Each of these KPIs provides unique insights that can paint a more detailed and nuanced picture of a fintech startup's performance and potential. Let's delve into them.

1. User Growth Rate: This KPI measures the speed at which a startup is acquiring new users. Rapid user growth can indicate market acceptance and a scalable product or service.

2. Active Users: The number of active users offers insights into user engagement and product value, which are critical for growth.

3. Customer Acquisition Cost (CAC): This metric calculates the cost of attracting a new customer. It's especially important for fintech companies, which often depend on scaling quickly. Learn more about the CAC in this guide.

4. Lifetime Value (LTV): This KPI estimates the total net value of a customer throughout the duration of their relationship with the company. A high LTV denotes increased profitability per customer. Learn more about the LTV (or CLV) in this guide.

5. LTV/CAC Ratio: This ratio gives a snapshot of customer relationship profitability. A higher ratio indicates a more profitable customer.

6. Churn Rate: The churn rate measures the number of customers who stop using a product over a specific period. A lower churn rate suggests customer satisfaction and product stickiness.

7. Burn Rate: This is the rate at which a company is spending its capital. It's a critical measure of a startup's sustainability and runway. Learn more about the burn rate in this guide.

8. Revenue Run Rate: This KPI projects a startup's future revenue based on current performance, offering a useful growth metric for fast-evolving fintech startups.

9. Transaction Volume and Value: For fintech startups involved in processing transactions, such as payments platforms, the volume and value of transactions can signify market share and acceptance.

10. Net Interest Margin (NIM): This is a profitability measure for fintech startups involved in lending or other interest-based services. It calculates the difference between interest income and interest expenses relative to the assets that earn interest.

11. Prepayment Rate: This is especially relevant for lending platforms. It measures how quickly borrowers are paying off their loans, which can impact interest income.

12. Default Rate: This measures the loans that are expected not to be repaid, providing an indication of the risk profile of a lending fintech's portfolio.

13. Gross Transaction Volume (GTV): GTV measures the total transaction volume in a given period, providing insights into a fintech's scale and market acceptance.

14. Regulatory Compliance Levels: Due to the importance of regulatory compliance in the financial industry, investors often scrutinize this KPI to assess a fintech startup's ability to navigate complex regulatory landscapes.

15. Profit Margin: As fintech startups mature, their profit margin becomes increasingly important for investors, providing insights into their potential profitability.

By understanding these KPIs, investors can form a comprehensive view of a fintech startup's health and future prospects. These metrics provide a foundation to inform investment decisions and apply the valuation methods discussed in the previous sections effectively.

Tech startups often face challenges when seeking accurate valuations that truly reflect their unique business models. Traditional valuation services can be frustrating, offering generic approaches that overlook the specific factors driving a startup's success. Finro offers a different approach.

At Finro, we recognize that tech startups require more than a standard valuation. We focus on understanding the complexities of your industry and the unique aspects of your business. Whether it’s your innovative revenue streams, niche market, or growth potential, our approach ensures these elements are thoroughly assessed.

Instead of long, drawn-out processes, we deliver precise and insightful valuations quickly, helping you make strategic decisions with confidence.

Expertise in Tech Startups: Finro is not just another valuation service. We specialize in tech startups, which means we understand the specific challenges you face. Whether your focus is SaaS, Fintech, Healthtech, or another tech sector, we tailor our valuation methods to capture the full scope of your business’s value. Our deep industry knowledge allows us to provide valuations that resonate with investors and support your growth plans.

Personalized, Cost-Effective Solutions: Quality financial consulting should be accessible, not a burden. Finro offers personalized valuation services at competitive prices, ensuring you receive top-tier analysis without straining your resources. Our flexible approach allows us to meet the needs of your startup today while preparing for future growth.

Rapid Turnaround Times: Timing is critical for startups, and we understand the need to act quickly. Finro is committed to delivering valuations swiftly, without compromising accuracy or depth. Our efficient process ensures you receive the vital information you need promptly, so you can move forward with confidence.

A Strategic Partner in Your Growth: Choosing Finro means more than just getting a valuation; it means partnering with a team that is genuinely invested in your success. We work closely with you to understand your vision, goals, and challenges, providing strategic guidance that goes beyond the numbers.

Our success stories and client testimonials highlight the real impact of our work in helping startups secure funding, refine their strategies, and achieve their growth goals.

Having the right valuation partner for your startup can make all the difference.

Finro offers a smarter, more tailored approach to valuations, combining industry-specific expertise, personalized service, cost-effective solutions, and rapid delivery.

We are more than just valuation consultants; we are your strategic partners in growth.

Let Finro help you unlock your startup’s true potential and navigate the complexities of the tech world with confidence.

Valuing a fintech startup requires a thorough understanding of the company's unique characteristics, market positioning, and growth potential.

While several valuation methods are available, the Discounted Cash Flow (DCF) and the Market Multiple methods are commonly used for fintech startups. These methods rely on the company's financial projections, growth potential, and comparable companies' valuations to determine an appropriate valuation.

In addition to valuation methods, investors should consider other key factors that can impact fintech startup valuation, such as market size, competition, regulatory environment, intellectual property, and management team. These factors can significantly impact the company's growth potential and risk profile.

Furthermore, assessing key metrics such as CAC, CLV, MRR, ARPU, NIM, burn rate, churn rate, GTV, etc., can provide valuable insights into the company's financial health and growth potential.

Innovation-Driven Disruption: Fintech startups disrupt financial sectors by prioritizing innovative tech, user experience, and rapid market growth.

Valuation Method Mix: Valuation balances art and analytics, combining DCF and comparative analyses with fintech-specific considerations like innovation rate.

Assessing Growth Potential: Growth potential is critical; considers user base, market size, and adaptability to forecast fintech's scaling capabilities.

Leadership Impact Significant: Team quality, expertise, and vision significantly influence fintech valuation, reflecting leadership's role in strategic success.

Critical Performance Metrics: Key metrics like user growth, CAC, LTV, and churn rate offer nuanced insights into fintech startups' performance and potential.

Valuing fintech startups involves assessing unique technology, market disruption potential, and forward-looking growth metrics.

Startups are valued using methods like DCF, market multiples, and consideration of growth potential and financial forecasts.

DCF projects future cash flows discounted to present value, adjusted for risk, to value mature startups with stable finances.

Use industry multiples from similar companies on the startup's revenue to estimate market valuation.