How To Value A Pre-Revenue Startup?

By Lior Ronen | Founder, Finro Financial Consulting

Stepping into the startup arena is a thrilling ride.

You've been up nights, tweaking and perfecting your big idea – your baby.

And here you are now, at a crossroads, facing one of the biggest questions: What's your startup's worth, especially when you haven't made a dime yet?

It's a head-scratcher, for sure.

Where do you even start with valuing something that's yet to bring in revenue?

How do you figure out a price tag that feels just right – not sky-high to scare off investors, but not so low that it undersells your potential?

Well, that's where we come in.

As the leading startup valuation firm, we’ll help gain a preliminary understanding of how to value a startup company with no revenue.

We'll break down various valuation methods, from quantitative ones like the Berkus Method and Scorecard Method to qualitative approaches involving Revenue and EBITDA multiples and even the nuanced Discounted Cash Flow method.

Pre-revenue startup valuation refers to estimating the value of a startup company that has not yet generated revenue, typically based on factors like the team, product, traction, market potential, and investor interest.

Valuing a pre-revenue startup, which is still in its early stages and not yet generating revenue, is more complex than valuing established businesses with a steady income. The valuation acts like a thermometer, indicating the startup's health and growth potential.

Various methods, both quantitative (like the Berkus and Scorecard Methods) and qualitative (such as Revenue and EBITDA multiples, and Discounted Cash Flow method), are used to estimate a startup's value. These methods account for the startup's potential future growth and returns, which are critical to investors, rather than current financial performance

Understanding Pre-Revenue Startup Valuation

Remember the moment your startup idea first sparked to life?

Maybe you scribbled down notes, drafted a prototype, or outlined a business plan.

Initially, it was all about potential, not profit.

This early phase, where you're building your product or service without generating sales, is what we call pre-revenue.

Your startup may not be earning yet, but that hardly means it lacks value. In fact, its real worth lies in its future potential, which is exactly what catches an investor's eye.

Investors are betting on what returns your startup could yield down the line.

Valuing your startup, therefore, becomes a critical exercise in quantifying this potential. It's essential for negotiating equity – the percentage of your startup an investor will own based on their investment.

Consider an investor ready to put $1 million into your startup.

A $4 million valuation means they get 25% ownership, whereas at $10 million, they'd only secure 10%. Clearly, your business valuation significantly influences your stake in your own company.

But how do you put a number on a business yet to see its first sale?

Traditional valuation metrics, centered around sales and profits, aren't much help here.

Fear not. We've got an array of methods tailored for valuing pre-revenue startups, and we're about to dive deep into them.

We'll examine both subjective methods, focusing on your startup's intrinsic qualities, and objective ones, grounded in financial projections and market comparisons.

Up next, we'll explore methods like the Berkus Method and the Scorecard Method, perfect for gauging your startup's unique appeal.

Then, we'll venture into more data-driven approaches, including the Discounted Cash Flow (DCF) method, adjusting our lens to the financial side of your startup's future.

Each valuation method has its perks and pitfalls. Stick with us to learn how to navigate these tools effectively, ensuring you can confidently discuss your startup's value with potential investors.

| Qualitative Methods | Quantitative Methods |

|---|---|

Qualitative Valuation Methods

In the realm of startup valuation, not everything can be measured with numbers. For pre-revenue startups, traditional financial metrics like sales or profits aren't available, so we need to use other factors to estimate the startup's worth. This is where qualitative valuation methods come into play.

So, what exactly are qualitative valuation methods?

Essentially, they are valuation techniques that consider subjective and non-numerical factors. These methods look at various aspects of your startup such as the strength of your team, the potential market size, the stage of development, and more.

While these factors might seem intangible, they can give a powerful indication of your startup's future potential. After all, a strong team, a well-developed product, and a large potential market can lead to significant revenue down the line.

In this section, we're going to focus on two popular qualitative methods used in pre-revenue startup valuation: the Berkus Method and the Scorecard Method.

Both methods offer unique ways of looking at your startup's value, taking into account a range of factors beyond just the financials.

So, are you ready to delve into the less tangible, but equally crucial, aspects of your startup's value? Let's begin with the Berkus Method.

Get your expert valuation now!

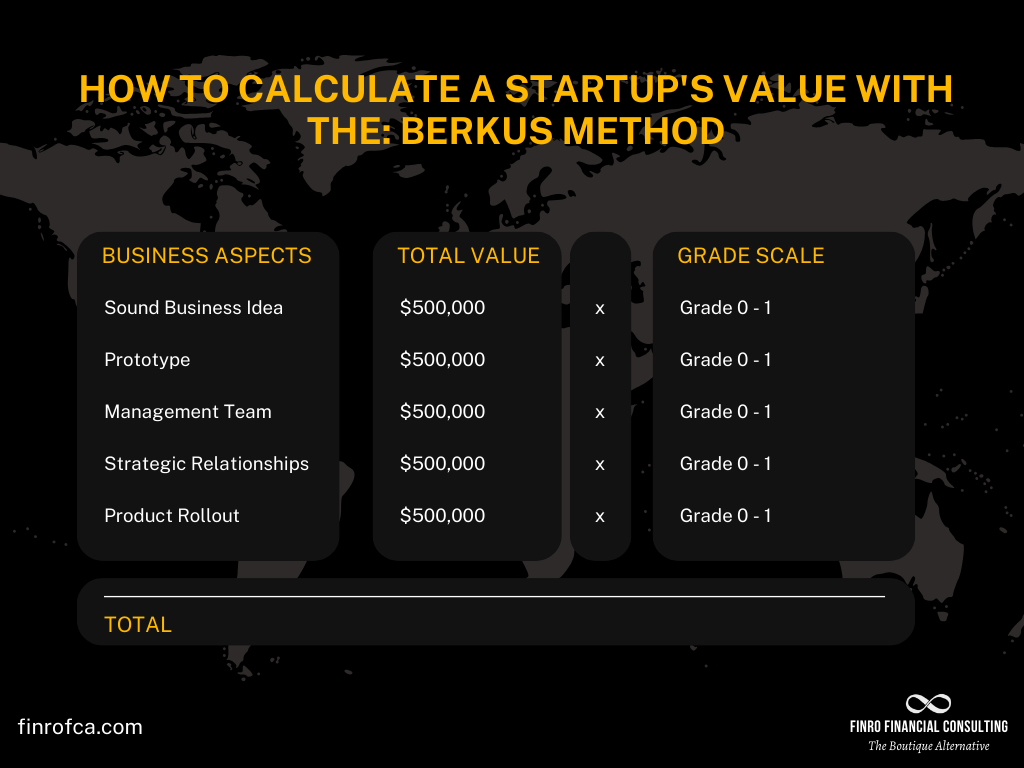

The Berkus Model

In the world of early-stage startups, the Berkus Method is a well-known valuation tool.

Created by renowned angel investor Dave Berkus, this method is designed to value pre-revenue startups that had the potential to reach $20 million within 5 years, based on qualitative factors.

This approach can be particularly useful for startups that don't have a long history of financial data to lean on.

It is usually used by angel investors, accelerators, and individual venture capitalists to value startups in the idea stage.

How to Use the Berkus Method

The Berkus Method offers a straightforward approach to estimating the value of a startup, focusing on its potential to earn $20 million in revenue within five years.

This method considers five key elements crucial to a startup's success: the soundness of the business idea, the strength of the management team, the quality of strategic relationships, the development stage of the product or prototype, and the establishment of sales channels.

Each of these elements can be assigned a value of up to $500,000, leading to a total maximum valuation of $2.5 million for an early-stage startup with no revenue.

However, this cap can be adjusted based on the average pre-seed valuation in the startup's specific niche or location, allowing for a more tailored valuation range.

To apply the Berkus Method, start by ensuring that the startup under evaluation aims to generate at least $20 million in revenue over the next five years. If so, this method is applicable.

The valuation process involves subjectively grading each aspect of the business, from management and product development to technology and strategic partnerships.

For example, management might be valued at $500,000, the product at $400,000, technology also at $500,000, providing a basic value of $500,000, and strategic relationships at $200,000.

This results in a pre-revenue startup's value of approximately $2.1 million, with the potential for investors to see a return of ten times their investment.

The Berkus Method simplifies the valuation of early-stage startups by assigning rough value estimates to different business components based on subjective assessment.

Individuals grading each aspect can increase or decrease the final valuation, emphasizing the importance of a strong management team, innovative product, and solid strategic relationships.

Adjustments to the valuation cap can be made to reflect the specific circumstances and expectations within a startup's niche or geographical location, offering a flexible and intuitive approach to understanding a startup's worth.

When to Use the Berkus Method?

The Berkus Method is best suited for very early-stage startups that are pre-revenue and do not have a lot of historical financial data.

If you're still developing your product or service and haven't started selling yet, the Berkus Method could be a good fit for your startup.

Berkus Method Pros and Cons

| Pros | Cons |

|---|---|

| Simple and easy to understand | May oversimplify the complexities involved in startup valuation |

| Based solely on qualitative aspects | Ignores financial risk, which is a common pitfall for startups |

| Easily adaptable to different circumstances, including geography, sector, and currency | The model's simplicity may not replace the need for comprehensive due diligence |

| Considers key risk areas that can make or break a company, encouraging risk management | Best suited for very early-stage, pre-revenue startups, and may not be appropriate for later-stage startups with recurring revenue streams |

| Provides a quick valuation method that is useful for founders and early-stage investors | The values can be subjective and are the result of negotiations, which can lead to conflicting interests between founders and investors |

The Scorecard Method

The Scorecard Method is a valuation methodology primarily utilized for early-stage, pre-seed, and seed startups that are yet to generate revenues. This technique evaluates a startup's worth by comparing it to benchmarks from similar startups and averaging out their pre-money valuations.

How To Use The Scorecard Method?

The Scorecard valuation method includes 4 primary steps:

1. Find the Average Pre-Money Valuation: You start by determining the average pre-money valuation for pre-revenue startups in the same region and business sector as the startup you're valuing.

2. Assign Factors: Next, you evaluate the startup based on various factors and assign it a score for each factor. The factors typically considered in the scorecard method are:

The strength of the Management Team (0–30%)

Size of the Opportunity (0–25%)

Product/Technology (0–15%)

Competitive Environment (0–10%)

Marketing/Sales Channels/Partnerships (0–10%)

Need for Additional Investment (0–5%)

Other (great early customer feedback) (0–5%)

These weights can be adjusted to reflect the specifics of the startup and the perspectives of the investors. The initial step in the Scorecard Method involves finding the average pre-revenue pre-money valuation within the region and business sector of the target startup.

3. Calculate Weighted Score: Then you calculate a weighted average of these scores to get a factor that you apply to the average pre-money valuation.

4. Multiply the Average Pre-Money Valuation by the Weighted Score: Finally, you multiply the average pre-money valuation by the weighted score to get the valuation for the startup.

When to Use the Scorecard Method

The Scorecard Method is particularly useful when comparative data from other startups is available.

Such data allows for a more accurate benchmarking process, facilitating a fairer estimation of a startup's value.

| Pros | Cons |

|---|---|

| Takes into account multiple factors impacting a startup's value | Requires comparable data from other startups |

| Allows for customization based on each startup's unique characteristics | Still requires subjective judgements |

| Provides a more holistic view of the business | May not fully capture the unique nuances of each startup, potentially leading to over or underestimation of its value |

Quantitative Valuation Methods

So far, we've talked about two ways to figure out how much a startup might be worth, even before it's started making money. These ways called the Berkus Method and the Scorecard Method, look at things like how good the team is or how big the market for the startup's product could be.

But what happens beyond the idea stage, and how do you value an early-stage startup with objective, measurable methods?

Well, there are four main ways to do that:

Revenue Multiple Method: This way is pretty straightforward. We take the money the startup is making from sales (this is called revenue), and then we multiply it by a certain number (a "multiple") to get our valuation. The number we use for the multiple usually depends on what other similar companies are worth.

EBITDA Multiple Method: This is pretty much the same as the Revenue Multiple Method, but instead of just looking at the money from sales, we also consider some of the startup's costs. This gives us a better idea of how much money the startup keeps from its sales.

Previous Transactions Method: Here, we look at how much people have paid recently for other similar startups. This gives us a good idea of how much someone might be willing to pay for our startup.

Discounted Cash Flow (DCF) Method: This is a bit more complicated. With the DCF method, we try to figure out how much money the startup will make in the future, and then we adjust these amounts to reflect their value in today's dollars.

Each of these ways has its advantages and disadvantages, and often, people will use a combination of them to better understand a startup's worth.

Let's look at each of them in more detail.

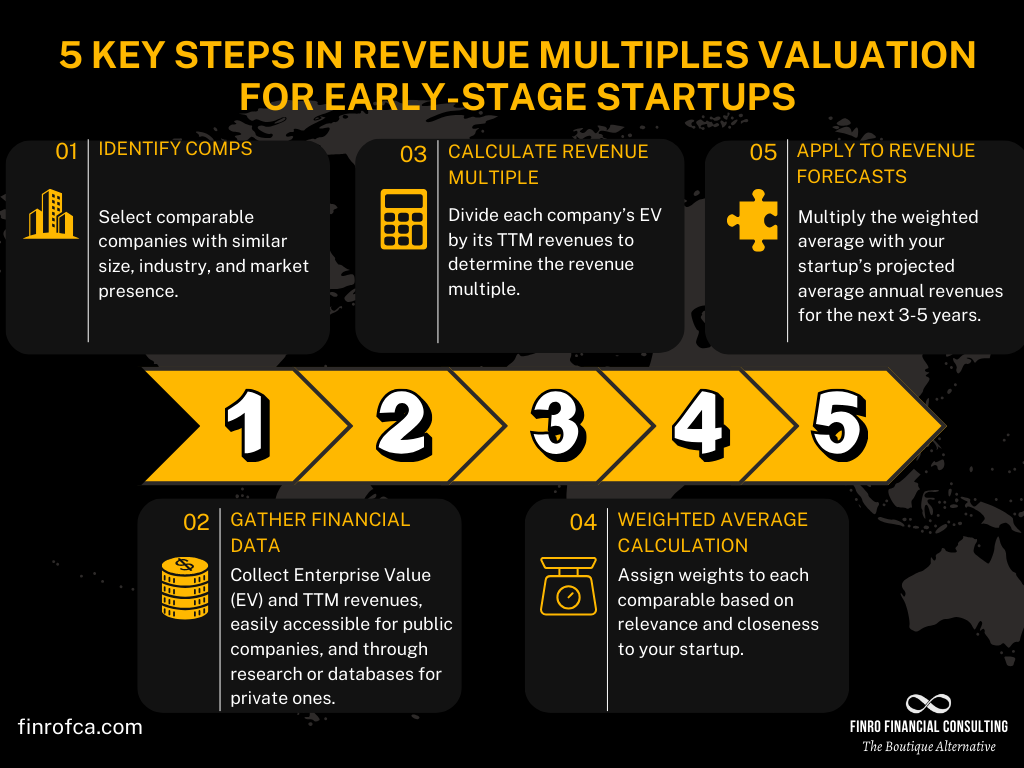

Revenue Multiple Method

Even though your startup might not yet be generating revenue, that doesn't mean it lacks value. The Revenue Multiple method can still be used as a reference point to anticipate a future valuation. This method, based on revenue figures, can give you a glimpse of your startup's potential worth once it starts generating income.

The revenue multiple represents the value of a startup in terms of its revenues. For instance, if a startup has a revenue multiple of 3x, it implies that the startup's value could be three times its annual revenue once it starts generating income.

This method is especially insightful for pre-revenue startups, helping you and potential investors understand the value proposition, even in the absence of current income.

For pre-revenue startups, applying the revenue multiple method involves some hypothetical considerations.

Step 1: Estimate Future Revenue

The first step in applying the revenue multiple method for a pre-revenue startup involves projecting the company's potential annual revenue. This is an educated guess based on various sources of information.

Market research: Study the market you're operating in or planning to enter. Understand the size of the market, the current demand, and the expected growth rate. This will give you a solid basis for estimating the revenue your startup could generate.

Business plan: Your business plan should contain detailed financial projections. Use these to estimate your future annual revenue. Make sure these projections are realistic and based on solid assumptions. If they seem too optimistic, you might need to revise them to avoid overestimating your future revenue.

Performance of similar startups: Look at the performance of other startups in your industry, especially those at a similar stage or with a similar business model. Their revenue figures can provide a useful benchmark for your own projections.

Step 2: Research Industry Multiple

The next step is to find the average revenue multiple for your industry. This comps analysis is the fundamental basis for the entire revenue multiple method (and EBITDA multiple) valuations is based on.

Financial databases: Many financial databases provide data on revenue multiples for different industries. These databases might require a subscription or payment, but the information can be valuable for getting an accurate industry multiple.

Industry reports: Some consultancy firms, market research companies, and financial institutions publish industry reports. These reports often contain valuable information about revenue multiples in different sectors.

Financial advisor: If you have access to a financial advisor, they can be a valuable resource. They can help you find and interpret information about revenue multiples in your industry.

Remember, the average industry multiple can fluctuate over time due to various factors, including economic conditions and industry trends. So, it's crucial to use the most recent data available.

Step 3: Calculate Potential Value

Once you have your estimated future revenue and the industry multiple, you're ready to calculate your startup's potential value.

To do this, simply multiply your estimated future revenue by the industry multiple. For example, if your estimated future revenue is $1 million and the industry multiple is 5x, your startup's potential value would be $5 million.

Keep in mind that this figure is just a projection. It's based on estimates and assumptions, which might not turn out to be accurate. As such, it should be used as a reference point rather than a definitive value. Be prepared to explain and defend your assumptions if you're using this valuation in discussions with potential investors or other stakeholders.

When to Use the Revenue Multiple

The revenue multiple method is best suited to startups that are generating steady revenue but are yet to see consistent profits. This is often the case with startups across various sectors, although it is particularly prevalent in the tech industry where companies often see substantial revenue before they become profitable.

Pros and Cons of the Revenue Multiple

The main advantage of the revenue multiple method is its simplicity. The process is easy to understand and it provides a clear estimate of a startup's value. Furthermore, it is an effective way of valuing a startup that is seeing rapid revenue growth, even if it is not yet profitable.

However, there are limitations to the revenue multiple method. It is not suitable for startups that are pre-revenue or have minimal revenue. The method also makes the assumption that all revenues contribute equally to the value of the startup. This is not always the case, as some revenue streams may be more sustainable or profitable than others.

Additionally, it can lead to overvaluing startups that have high revenues but low or negative profits. Lastly, it doesn't take into account other important factors such as the startup's growth rate, market potential, or profitability - all of which can significantly influence the value of a startup.

It is, therefore important to use this method alongside other valuation methods to gain a more comprehensive view of a startup's value.

| Pros | Cons |

|---|---|

| Simple and straightforward to calculate | Not suitable for pre-revenue or minimal revenue startups |

| Effective for startups with rapid revenue growth | Assumes all revenue contributes equally to value |

| Relatively objective as revenue is hard to manipulate | Can overvalue high-revenue, low-profit startups |

| Useful for startups with consistent but not yet profitable revenue | Doesn't consider growth rate, market potential, or profitability |

While the Revenue Multiple method offers a straightforward way to estimate your startup's value based on its revenue figures, it might not capture the complete financial picture, especially for startups that have started generating profits.

If your startup has reached a point of consistent profitability, another quantitative method, known as the EBITDA Multiple method, could provide a more accurate valuation.

This method factors in earnings before interest, taxes, depreciation, and amortization, offering a deeper understanding of your startup's financial health and potential for growth. Let's delve into the EBITDA Multiple method next.

EBITDA Multiple Method

While the EBITDA multiple method is commonly used for established businesses with significant earnings before interest, taxes, depreciation, and amortization (EBITDA), applying this method for pre-revenue startups requires some modifications and creativity.

How To Use The Revenue Multiple Method?

Step 1: Estimate Future EBITDA

Estimating future EBITDA for your pre-revenue startup involves projecting the earnings of your startup before taking into account interest, taxes, depreciation, and amortization.

To make these projections, you should conduct a detailed review of your business plan, taking into account factors like your startup's growth strategy, expected sales, and operating costs.

Industry benchmarks and the financial performance of similar companies in your sector should also inform these projections. It's important to remember that these are just estimates and actual future earnings may differ.

Therefore, it's crucial to be realistic and conservative in your projections, so as not to overinflate the potential value of your startup.

Step 2: Research Industry EBITDA Multiple

The next step involves identifying the EBITDA multiple commonly used in your industry.

EBITDA multiples differ across industries due to factors like risk, growth prospects, and profitability. They are typically found in industry reports, financial databases, or with the assistance of a financial advisor.

As a rule of thumb, high-growth or high-risk industries tend to have higher EBITDA multiples. Identifying the correct EBITDA multiple is crucial as it can significantly impact your startup's estimated value.

Step 3: Calculate Hypothetical Value

Once you have your projected EBITDA and the industry multiple, the next step is simple arithmetic. You multiply the two together to estimate the hypothetical value of your startup.

It's important to note that this is just a projection based on your assumptions and the information available at the time of calculation. As such, the projected value may not reflect the actual value that potential investors may assign to your startup.

This is why the EBITDA multiple method should be used as a guide rather than a definitive measure of your startup's worth.

Remember, these calculations are based on a multitude of assumptions and are a projection of a potential future state.

They can help you gain an understanding of your startup's potential worth but should be used in conjunction with other methods and market feedback to derive a more comprehensive understanding of your startup's value.

Pros and Cons of the EBITDA Multiple

Keep in mind that this method is dependent on the accuracy of your projections. The further out you're forecasting, the less accurate your projections will likely be, which can introduce significant uncertainty to the valuation. It's crucial to be able to justify your assumptions, particularly to potential investors who may scrutinize your forecast.

The EBITDA multiple method, while valuable, may not be the best fit for all pre-revenue startups, particularly those in high-growth tech sectors where traditional EBITDA multiples might not reflect the startup's potential growth and market opportunity. Therefore, this method is often used in conjunction with other valuation methods to cross-verify the estimated value or to provide a range of potential values.

Remember, all valuation methods are just tools to estimate the value of your business. The real value of your startup will be determined in the marketplace when you negotiate with investors.

Keep an open mind and be prepared to discuss and defend your business's valuation and the assumptions that support it.

| Pros | Cons |

|---|---|

| Based on Industry Standards This method aligns your startup valuation with the broader industry standards, providing a potentially more realistic valuation. |

Based on Projections Since a pre-revenue startup does not have actual EBITDA figures, this method relies heavily on projections, which can be inaccurate and subject to change. |

| Accounts for Profitability By considering EBITDA, this method goes beyond just revenue and takes into account projected profitability. |

May Overlook Potential For startups in high-growth industries, the EBITDA multiple method may underestimate the startup's potential, especially if the industry's average EBITDA multiple is low. |

| Straightforward Calculation Once you have projected EBITDA and the industry multiple, the calculation is straightforward. |

Not Suitable for All Industries For some industries, especially in the tech sector, the EBITDA multiple method may not be as applicable or reflective of the startup's value. |

| Provides a Benchmark This method provides a benchmark against which future performance can be measured. |

Requires Financial Expertise Deriving reasonable projected EBITDA and understanding the industry EBITDA multiple requires a certain level of financial expertise. |

Having delved into the EBITDA Multiple method, a more advanced valuation method for startups with consistent profits, it's time to consider a method that brings us closer to market realities.

The Previous Transactions Multiple method allows us to leverage comparable past transactions in the industry to derive a potential valuation for the startup.

This method, which grounds our valuation in real-world data, can offer a more tangible reference point for investors and founders alike. Let's proceed with an exploration of the Previous Transactions Multiple method.

The Previous Transactions Multiple Method

After discussing the Revenue and EBITDA Multiple methods, we're now shifting our focus towards the Previous Transactions Multiple method, which provides another angle for valuing pre-revenue startups.

This method uses the valuation multiples derived from previous investment transactions in similar companies, instead of basing the value on your own startup's revenues or EBITDA. This approach takes into consideration the actual market conditions and the price investors have been willing to pay for similar companies.

The process of applying the Previous Transactions Multiple Method involves the following steps:

1. Identifying Comparable Transactions

The first step is identifying comparable transactions, meaning finding similar startups that have recently had investment transactions.

These startups should be similar in terms of their industry, market size, growth stage, business model, and other relevant factors. Information about these transactions can usually be found in databases such as Crunchbase, Pitchbook, or other industry reports.

2. Determining the Transaction Multiple

After identifying the transactions, the next step is to determine the transaction multiple. This could be based on a variety of factors, such as revenue or EBITDA, depending on what information is available for the comparable startups. These multiples reflect the ratio of the company's valuation to the chosen metric.

3. Applying the Multiple

After identifying the appropriate multiple, apply it to your own startup's estimated future revenues or EBITDA (depending on which was used in step 2). This gives you an estimation of your startup's value.

It's important to remember that while the Previous Transactions Multiple Method can provide valuable insights, it has its pros and cons.

On one hand, it accounts for market conditions and the price investors have been willing to pay for similar startups. However, its effectiveness is limited by the availability of comparable transactions, and it may not account for unique aspects of your startup that could affect its value.

| Pros | Cons |

|---|---|

| Reflects real market conditions | Dependent on the availability of comparable transactions |

| Incorporates prices investors have been willing to pay for similar startups | May not account for unique aspects of your startup |

| Can be a relatively simple calculation if enough data is available | Can be difficult to find exact matches or sufficiently similar startups |

In the next section, we'll discuss another valuation method - the Discounted Cash Flow (DCF) method, which is more focused on the future financial performance of your startup. This method provides a different perspective and completes our understanding of pre-revenue startup valuation.

Discounted Cash Flow (DCF) Method

The Discounted Cash Flow (DCF) method is a valuation approach that uses future free cash flow projections and discounts them, using a required annual rate, to arrive at a present value estimate. If the present value arrived at is higher than the current cost of the investment, the opportunity may be a good one.

For a pre-revenue startup, using the DCF method can be challenging as it requires estimating future free cash flows. However, if you have a solid business plan and a clear path to profitability, it could be a viable option.

Here's how you can apply the DCF method to a pre-revenue startup:

1. Project Future Cash Flows

This step involves creating detailed projections of future cash flows. These projections should take into account potential revenues, operating costs, capital expenditures, and changes in working capital. Remember, the further into the future the projections, the more uncertainty they carry.

2. Determine Discount Rate

Next, you'll need to determine the discount rate. This rate should reflect the riskiness of the cash flows. For startups, which are typically riskier, the discount rate would usually be higher. The most common way to do that is by using the WACC.

3. Discount the Cash Flows

Now, apply the discount rate to the projected future cash flows to bring them to present value terms. The rationale behind this is that a dollar today is worth more than a dollar in the future.

4. Sum up the discounted cash flows

Add up the discounted cash flows to get the total present value of the startup.

It's important to note that the DCF method, while rigorous and theoretically sound, comes with its own set of challenges and limitations. It relies heavily on the accuracy of projections, which can be difficult for pre-revenue startups, and it can be sensitive to changes in assumptions. However, when done properly, it can provide a thorough assessment of a startup's financial potential.

While this gives you a general overview of the Discounted Cash Flow (DCF) method, it's a complex process that we've covered in much more detail in another article. For a more in-depth understanding of the DCF method, its intricacies, and how to effectively implement it, be sure to check out our detailed guide on Understanding the Discounted Cash Flow (DCF) Method.

Conclusion

Valuing a pre-revenue startup isn't an easy task, but it is crucial for understanding the financial potential of your venture and attracting investors. We've discussed several methods in this guide, each with its own advantages, limitations, and ideal use cases.

Qualitative methods, such as the Berkus Method and the Scorecard Method, offer a valuable approach when financial data is limited or uncertain. They focus on qualitative aspects of the business like the strength of the management team, the size of the opportunity, and the product or technology. These methods can be more subjective, but they provide a valuable perspective that can complement more number-driven approaches.

On the other hand, quantitative methods including the Revenue Multiple, EBITDA Multiple, Previous Transactions Multiple, and DCF methods, rely more heavily on financial metrics. They require more data and, in some cases, a certain level of financial performance. But they offer a more rigorous, market-based or finance theory-based approach to valuation.

It's often beneficial to use multiple methods to triangulate a realistic valuation range. This approach can provide a more comprehensive view of your startup's value and can cater to investors who may have different preferences for valuation methods.

Here's a summary table that compares the different methods we've discussed:

Remember, valuation is as much an art as it is a science. It's all about presenting a credible story about your startup's potential, backed by solid numbers or strong qualitative factors.

And, while getting your startup valuation right is important, focusing on building a profitable, scalable business should always be your top priority.

Key Takeaways

Future Potential Valuation: Pre-revenue valuation reflects future potential, considering elements like team quality, product stage, and market size.

Berkus Method Application: The Berkus Method values early-stage startups by assigning monetary worth to factors like idea soundness and team strength.

Scorecard Method Benchmarking: The Scorecard Method benchmarks against similar startups, using weighted scoring on various qualitative factors.

Quantitative Methods Overview: Quantitative methods like Revenue and EBITDA Multiples project valuations based on financial metrics adjusted for startups.

DCF Method Explained: The DCF method is complex, focusing on projected future cash flows and discount rates, tailored to a startup’s specifics.

Answers to The Most Asked Questions

-

Estimating a startup's worth before it has generated revenue, focusing on potential, team, product, and market size.

-

Through methods like Berkus and Scorecard, focusing on qualitative aspects like team strength and market potential.

-

Pre-money valuation is before investment; pre-revenue is before generating sales, focusing on future potential.