The Comparables Method Of Startup Valuation, Explained

By Lior Ronen | Founder, Finro Financial Consulting

Estimating a startup's valuation isn't easy. This is especially true for early-stage startups, which are often pre-revenue and have very limited if any, actual financials.

The challenge is not just in building financial projections for a company, but figuring out its growth path, but also in valuing such a business.

So, how do we tackle this challenge?

There’s a reliable and straightforward solution: the comparables valuation method.

In the upcoming sections, we’ll explore the fundamentals of startup valuation and dive into the comparables valuation method.

You'll learn how to apply this method to calculate a company's valuation effectively.

We'll also discuss how to identify the right comparables for your business and highlight the nuances in applying the Comparables method to early-stage versus late-stage startups.

Without further ado, let's dive headfirst into the world of the Comparables valuation method, unraveling its intricacies and discovering how it can be a game-changer in startup valuation.

The Comparables Valuation Method, also known as the Multiples method or the comparable company analysis method, is a valuation method used to estimate the value of a company by comparing it to similar businesses in the same industry. This method is useful for startups in all stages and brings useful market data to the deal table.

It is exceptionally versatile and suitable for businesses of any niche or development stage. From pre-revenue and early-stage startups that can utilize revenue multiples, to more mature companies nearing positive EBITDA, which can adopt both revenue and EBITDA multiples for valuation, this method offers a comprehensive framework. Its adaptability makes it a crucial tool for startup valuation across various growth phases.

- What is Startup Valuation?

- What is Comparables Valuation?

- Identifying the Right Comparables for Startup Valuation.

- Applying Revenue Multiples in Early-Stage Startup Valuation.

- Expanding the Multiples Method for Late-Stage Startups.

- Leveraging Previous Transactions in Valuation.

- Final Synthesis: Integrating Valuation Methods and Next Steps.

What is Startup Valuation?

Startup valuation is the process of determining the worth of a new business venture.

Before engaging with investors to raise funds, startups already need to have a valuation estimate ready.

Why?

Because they need to establish fair terms for what percentage of ownership to give up and how many dollars they hope to raise by selling that equity.

Let’s say you want to sell your bike on Facebook Marketplace. Potential buyers will first ask how much you want to sell it for and what model/year it is.

Similarly, investors want to know the valuation founders place on their startup and the dollar amount they seek for a set portion of equity.

Having an upfront valuation ready and a desired fundraising total allows both parties to initially assess if the deal makes sense before spending time negotiating finer details.

But there's more to it than just setting a number.

Like a bike's price, your startup's valuation depends on several factors: market potential, team expertise, proprietary technology, and proven traction.

Showing a hockey stick growth chart is not enough to convince anyone. A good valuation, like that we build here in Finro, shows investors the real drivers behind the startup’s growth.

Investors must understand these factors and how they contribute to your company's worth. And you need to show it. Being prepared with a valuation demonstrates seriousness and realistic market understanding, which can significantly influence investor confidence.

However, it's also important to recognize that valuation isn't a one-size-fits-all figure.

Different startups in different niches and stages require different methods like discounted cash flow, revenue multiple, and EBITDA multiple (also known as EV EBITDA). We often use a mix of methods to fit the startup’s case.

Get your expert valuation now!

Qunatitative vs. Qualitative Valuation Methods

Valuation methods fall into two main categories: qualitative and quantitative.

Qualitative methods focus on non-financial, subjective factors and are more flexible but less predictable, ideal for idea-stage startups or those approaching angel investors, accelerators or pre-seed VCs.

These methods focus on subjective aspects like team quality, market potential, product uniqueness, and operational capabilities. The startup's value is inferred from these qualitative assessments, benchmarked against similar startups in the industry.

The primary qualitative valuation methods are:

The Payne Scorecard Method

The Risk Factor Summation Method

Quantitative methods, on the other hand, rely on financial data, are more complex and predictable, and are better suited for startups from seed stage and on.

These methods rely on thorough financial modeling, headcount forecasting, business planning, and historical financial analysis if the startup has any.

The primary quantitative valuation methods include:

The Discounted Dividends Method

And others

The comparable valuation method that we discuss in this article is a relative valuation method that falls under the quantitative methods and applies across the board, from seed startups to late-stage startups.

Before diving deeper into the main topic of this article, let’s quickly see when we should use each method.

Picking The Right Valuation Method

After learning about the difference between qualitative and quantitative valuation methods, it's important to understand how these methods apply to startups at different stages of their growth.

In the earliest phase, when a startup is just an idea or in the pre-seed stage, the main focus is on validating the concept and getting ready to launch.

Since there's not much financial data to analyze, startups at this stage don't usually set a specific value. Instead, they might use funding options like SAFE (Simple Agreement for Future Equity) or Convertible Notes, where the valuation isn’t immediately decided.

As the startup develops into the pre-seed and seed stages, it begins to take shape. Here, they are building their first product versions and shaping their business model. Valuation becomes more relevant.

Angel investors might prefer qualitative methods, like the Berkus Method, that focus on the startup's potential rather than just numbers. Venture capitalists, however, might start looking at quantitative methods, which are based on financial data, to decide the startup's value.

Moving to the Series A and B stages, startups are refining their products and understanding their market better. At this point, methods like the Comparables method, which looks at revenue and profits, become useful. These methods help in making more structured financial predictions about the startup’s future.

Finally, in the Series C stage and beyond, when startups are more established and have a clear path to profitability, a mix of various valuation methods is used. This includes methods like Discounted Cash Flow and Net Asset Value, providing a more comprehensive and accurate valuation.

Understanding these stages helps us see why the Comparables method, which we’ll explore next, is particularly relevant for startups that have moved beyond the early development phases and have more substantial financial data.

| Stage | Characteristics | Valuation Methods |

|---|---|---|

| Idea to Pre-Seed | Idea validation, proof of concept, pre-revenue. | Unpriced rounds (SAFE, Convertible Notes), no immediate need for valuation. |

| Pre-Seed and Seed | Initial development, possibly pre-alpha/alpha stage, clarity on business model. | Qualitative methods (Berkus, Risk Factor Summation, Payne Scorecard) for angels; Quantitative methods (Venture Capital Method, Comparables) for VCs. |

| Series A and B | Late stage of alpha/beta, possibly MVP, finding product-market fit, beginning to understand business model. | Comparables method (revenue and EBITDA multiples), more structured financial and business projections. |

| Series C to Beyond | Mature startups, clear path to profitability, substantial business and financial data. | Comparables, Discounted Cash Flow (DCF), Net Asset Value (NAV), multiple methods for accuracy and bias reduction. |

What Is Comparables Valuation?

In the previous sections, we learned what a startup valuation is, the differences between quantitative and qualitative valuation methods, and how to pick the right method for your case.

In this section, we’ll start diving into the world of comparable valuation methods.

But what is the comparables valuation method?

The comparables valuation is a market approach to valuation where we use real market data to calculate the value of a company, by analyzing its peer group. It’s one of the quantitative methods, which uses a broad set of assumptions, calculations, and market research to calculate the value.

Sounds weird. What does it mean?

We look at the financial ratios of relevant comparable companies and apply these to our case to calculate the value of our company.

What are financial ratios, and who are the comparable companies we should use?

Ratios, also known as multiple; hence, this method is often named the multiples method, or EV multiples, are financial tools that help us compare different companies while neutralizing their size and market conditions.

The comparables we choose are typically market leaders, peers within your business category, suppliers, clients, or any entity with a business model and operational characteristics similar to the company we value.

The selection of comparables is a nuanced process, as it involves understanding both the macro and micro aspects of the business environment, including industry trends, competitive landscape, and specific business operations.

How do we do it?

The comparables method values the company by combining three data points:

Projected revenues or EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization).

Comparables’ revenue multiple, which is the ratio between a company’s value to its annual revenue.

Comparables’ EBITDA multiple is the ratio between a company’s value and its annual EBITDA.

What makes the Comparables Method particularly effective is its reflection of the current market conditions and how similar companies are valued by investors and the market at large.

The great 2 advantages of this method are:

Bring real market data to the table. Since the method includes multiple peers, the valuation discussion is automatically elevated to real data, not just theories.

Flexible and easily applied for every business. Since the method uses market data of revenue, EBITDA, and sometimes other multiples and applies them to our company’s projection, it can be used with pre-revenue startups, early-stage startups, late-stage, mature companies, and basically every business that has comparables and financial forecasts.

In this section, we learned what is the comparables valuation method, how to use it (at a high level), and set the ground for the following sections.

In the next sections, we’ll see how to identify the rights comparables for our analysis, how to calculate the comparable valuation for early-stage vs. late-stage startups, what the difference is between that and the DCF, and more.

Comparables Method vs. The DCF Method

The Comparables Valuation Method differs significantly from the Discounted Cash Flow (DCF) method in its foundational approach to valuing a business.At its core, the Comparables Method is market-oriented, deriving value from the financial metrics of similar companies in the industry. This approach makes it particularly adaptable and relevant for startups at various stages, as it mirrors current market sentiments and trends.

In contrast, the DCF method is intrinsically focused on a company’s internal financial health, projecting future cash flows and discounting them to present value. This internal focus requires extensive financial forecasting, rendering DCF more suitable for mature companies with predictable financial trajectories.

While the Comparables Method provides a market-centric valuation perspective, the DCF method offers a detailed internal financial analysis, each serving different purposes in the spectrum of business valuation.

| Criteria | Comparables Method | DCF Method |

|---|---|---|

| Basis of Valuation | Market-based. Uses financial ratios of similar companies. | Cash flow-based. Projects future cash flows and discounts them to present value. |

| Applicability | Broad, especially effective for startups at any stage, including those without positive cash flow. | Best for companies with predictable and stable cash flows. |

| Complexity | Relatively simpler, as it relies on available market data. | More complex due to the need for detailed financial forecasting. |

| Data Requirement | Requires financial data of comparable companies and financial projections of specific business' aspects. | Requires detailed financial projections, detailed financial data of comparable companies, and financial market data. |

| Market Relevance | High. Reflects current market conditions and investor sentiment. | Lower in rapidly changing markets. |

| Ideal Use Case | Startups without a long financial history; when market comparables are readily available. | Mature companies with stable and predictable cash flows; when internal data is reliable and comprehensive. |

Identifying the Right Comparables for Startup Valuation

The cornerstone of the comparables valuation approach is the comprehensive comparable companies analysis, often referred to as comps.

This methodical process involves selecting and examining companies similar to the one being valued and is crucial in achieving an accurate and market-relevant valuation.

In building a robust list of comparables, it's essential to include a diverse range of companies. This list should encompass market leaders and peers, offering insight into industry benchmarks and standards.

Additionally, it's important to consider both direct and indirect competitors, as well as business partners, to understand the competitive landscape and market dynamics.

Companies operating under similar business models, regardless of their market segment, should also be included to ensure a comprehensive view of potential market positions and strategies.

What is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It's a financial metric used to assess a company's operating performance by focusing on the earnings generated from its core business operations.EBITDA is calculated by taking the company's net income and adding back interest, taxes, depreciation, and amortization expenses. This addition is significant because it removes the effects of financing and accounting decisions, providing a clearer picture of the company's operational efficiency and profitability. By excluding interest and taxes, EBITDA mitigates the impact of different capital structures and tax rates, allowing for a more direct comparison of companies regardless of these variables. Similarly, adding back depreciation and amortization expenses adjusts for the varying costs and methods of fixed assets and intangible assets accounting over time.

As a result, EBITDA is often used by investors and analysts to compare the financial performance of different companies within the same industry, especially when evaluating potential investments or acquisitions. It helps in understanding a company's ability to generate cash flow from business operations, which is crucial for assessing its financial health and growth potential.

However, it's important to note that EBITDA does not provide a complete view of a company's financial situation, as it doesn't account for capital expenditures or changes in working capital, which are critical for understanding a company's overall financial performance.

Read more

Essential Data Points in Comps Analysis

A thorough comps analysis requires careful consideration of key data points, including:

Company Name: Essential for context and relevance in the analysis.

Company Symbol: Important for public companies, aiding in information validation.

Valuation Metric: Use the latest funding round valuation for private companies, and Enterprise Value (EV) or market capitalization for public companies.

Revenues: The most recent annual revenues or estimates for private companies, and Trailing Twelve Months (TTM) revenue for public companies.

EBITDA: Typically for public companies, using TTM EBITDA, acknowledging the challenge of obtaining this data for private companies.

Beta: A measure of investment volatility relative to the market, used in specific valuation methods such as CAPM. An industry average might be used as a substitute for private companies. Beta is a primary component of the company's discount rate (or WACC) used in specific valuation methods.

Market Capitalization and Debt: These are crucial for understanding equity and debt ratios, particularly for DCF analysis. Industry averages can be used as estimates for private companies.

The choice of different multiples in the valuation process largely depends on the startup's stage of development. Revenue multiples are generally more suitable for early-stage startups, especially when there is a lack of extensive data or when positive EBITDA is not projected in the near future.

For later-stage or mature companies, a combination of both revenue and EBITDA multiples is often employed, particularly when there is an existing or expected positive EBITDA. Additionally, incorporating multiples from previous transactions in the same niche or involving comparable companies can significantly enhance the valuation by adding another layer of market insight. This approach is relevant and beneficial for both early and late-stage companies.

With a clear framework for selecting and analyzing comparables, we are now equipped to explore the specifics of applying these methods across different startup stages, ensuring a nuanced and effective valuation process.

Key Elements In Comparables Valuation

Effective comparables valuation hinges on several key elements that together provide a nuanced and comprehensive assessment of a startup's value. This process involves critical financial, market, and operational evaluations, each contributing significantly to an accurate valuation.The following aspects are crucial in shaping a well-rounded and reliable comparables valuation:

1. Selection of Comparable Companies: The accuracy of a comparables valuation largely hinges on choosing the right set of comparable companies. These companies should be similar in size, industry, growth stage, and market conditions to provide a relevant benchmark.

2. Financial Metrics and Multiples: Key financial metrics such as revenue, EBITDA, and net income are crucial. The selection of appropriate multiples (e.g., Price-to-Earnings, Enterprise Value-to-Revenue, Enterprise Value-to-EBITDA) based on these metrics is vital for a fair comparison.

3. Market Conditions and Trends: Understanding current market conditions and industry trends is essential to contextualize the valuation. This includes considering the economic climate, regulatory environment, and technological advancements that could impact the companies being compared.

4. Historical and Projected Performance: Both historical performance and future projections of the comparable companies need to be examined. This helps in understanding not just where the companies have been, but also where they are expected to go in terms of growth and profitability.

5. Operational Similarities and Differences: Beyond financials, operational aspects such as business model, customer base, geographical presence, and management quality should be considered. These factors can have significant implications for valuation, as they contribute to the overall health and potential of the business.

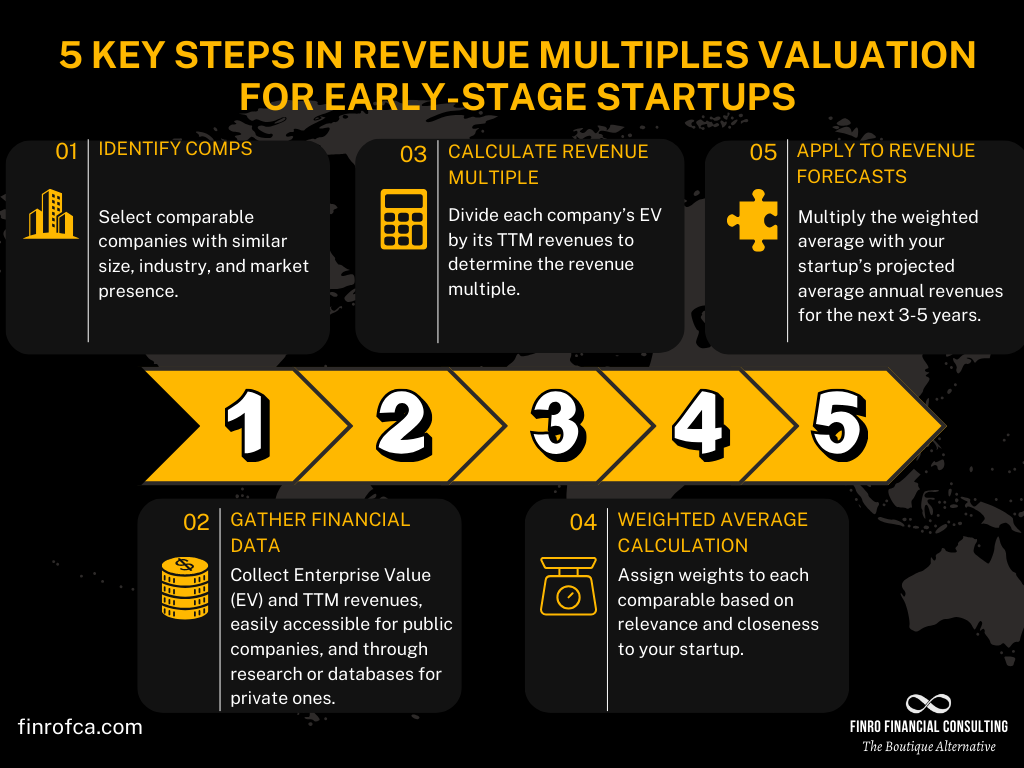

Applying Revenue Multiples in Early-Stage Startup Valuation

In early-stage startup valuation using the comparables method, the revenue multiple is a key financial ratio. This approach is particularly suited for startups that are in their early stages, have negative free cash flow, or are yet to achieve positive EBITDA.

Step 1: Building a Comparable Companies Analysis

The initial phase involves creating a comparable companies analysis (comps analysis). This analysis encompasses gathering financial metrics from similar companies, focusing on their Enterprise Value (EV) and Trailing Twelve Months (TTM) revenues and EBITDA. The revenue multiple is then calculated by dividing each company’s EV by its TTM revenues (EV/Revenues, also known as EV sales).

Step 2: Compiling a List of Comparables

The process starts with identifying potential comparable companies. This list should include direct competitors, peer companies, market leaders, and startups with similar business models operating in the same niche.

Step 3: Gathering Financial Information

For Public Companies: Financial data for public companies is more accessible, often available on financial news websites like Yahoo Finance. Here, you can find the latest EV and TTM revenues under the “statistics” section of the company’s page. If not available on Yahoo Finance, alternative sources include Morningstar, Seeking Alpha, or the company’s investor relations page.

For Private Companies: Gathering data for private companies can be more challenging, as such information is not always publicly available. However, valuations and revenue figures are often released during funding rounds or in official press releases. If direct information is not available, databases like Forge, Pitchbook, PrivCo, and CBInsight can be valuable resources.

Step 4: Creating a Weighted Revenue Multiple

Once you have a list of comparables and their revenue multiples, the next step is to determine the weighting of each company in the overall average. This weighting should reflect the closeness of each company to the one being valued. A weighted average of these multiples provides a more tailored and relevant metric.

Step 5: Applying the Weighted Multiple to Revenue Forecasts

Finally, apply this weighted average multiple to the startup’s projected average annual revenues over the next 3 to 5 years. This approach accounts for the expected growth rate, ensuring that the valuation reflects the startup’s future potential rather than just its current position.

Having explored the nuances of applying revenue multiples in valuing early-stage startups, we now turn our attention to the valuation complexities of late-stage startups.

In this next phase, the valuation process often requires a more intricate approach as these companies typically exhibit more substantial financial data, including positive EBITDA in some cases.

We will delve into how the multiples valuation method is adapted for late-stage startups, considering their advanced business development stage and more established market presence, to ensure a comprehensive and accurate valuation.

Expanding the Multiples Method for Late-Stage Startups

Building upon our understanding of the revenue multiples used for early-stage startups, we now explore how this method evolves for late-stage startups and mature companies, especially those with positive EBITDA.

For these more established entities, incorporating both EBITDA and revenue multiples enhances the valuation accuracy.

Integrating EBITDA into the Valuation Framework

While the revenue multiple remains a key component, the addition of the EBITDA multiple is what sets apart the valuation of late-stage startups.

This multiple is calculated similarly to the revenue multiple but focuses on the company’s EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization).

Here, the Enterprise Value (EV) is divided by the Trailing Twelve Months (TTM) EBITDA, providing insight into the company's profitability.

A Dual-Faceted Approach to Valuation

The valuation process for late-stage companies mirrors the earlier stages but with additional depth:

Gathering Comprehensive Financial Data: Alongside EV and sales data, it is crucial to include EBITDA figures in the analysis to capture a fuller financial picture.

Calculating Dual Weighted Averages: Once the comparable company analysis yields a set of multiples, the focus shifts to forming two weighted average figures — one for EV/sales and another for EV/EBITDA.

Applying Multiples to Financial Forecasts: The derived EV/Sales multiple is applied to the company’s revenue forecast, while the EV/EBITDA multiple is used with the EBITDA forecast. This dual application ensures a more rounded assessment of the company’s value, accounting for both its revenue streams and operational profitability.

By adapting the multiples method to encompass both revenue and EBITDA multiples, the valuation of late-stage startups and mature companies becomes more robust, reflecting the complexities and financial maturity of these businesses.

Moving from the use of revenue and EBITDA multiples, we now turn to the Previous Transaction Multiples Method. This approach leverages actual market transactions to inform startup valuations, offering a real-world perspective.

Next, we'll detail how to construct and apply this method, utilizing historical transaction data as a key valuation tool.

EV, or Enterprise Value, is a financial metric that reflects the total value of a company, encompassing more than just its market capitalization. It is designed to provide a comprehensive picture of a company's overall worth.

To calculate EV, you start with the company's market capitalization (the total value of its outstanding shares) and then add outstanding debt and subtract cash and cash equivalents. This formula accounts for the company’s debt and cash levels, which are crucial for understanding the true economic value of the company.

By including debt, EV acknowledges that a potential acquirer would need to take on the company's debt obligations. Similarly, subtracting cash and equivalents reflects the idea that a new owner could use the company's cash to offset a portion of the acquisition cost.

EV is particularly useful in comparisons across companies and industries because it provides a more holistic view of a company's value than market capitalization alone. It is widely used in financial analysis, including in the valuation of companies for mergers and acquisitions, and in calculating various financial ratios like EV/EBITDA.

Leveraging Previous Transactions in Valuation

The Previous Transactions method, sharing similarities with the multiples approach, utilizes real-market transaction data to gauge the value of a company. This method is grounded in the prices that buyers have historically been willing to pay and sellers have accepted, offering a pragmatic perspective on market valuations.

Data Collection Challenges and Strategies

Gathering accurate and comprehensive data for this method can be challenging. While deal sizes are often reported in public press releases accompanying the announcement of the transactions, these announcements typically do not disclose full deal terms but only the headline figures.

Consequently, it is necessary to pair these deal sizes with financial metrics like annual revenues or EBITDA for a complete picture. However, this financial information is frequently published separately, either in earlier or subsequent media reports, and may require extensive research to compile.

Finding Information on Previous Transactions

Despite the challenge, the effort to collect this data is often rewarding. Public sources and media publications can be rich sources of information. For transactions where data is partially reported or not publicly disclosed, private market platforms such as Pitchbook or PrivCo become invaluable.

These platforms specialize in financial data and offer access to detailed transaction information, albeit often at a cost.

This method’s reliance on past transaction data provides a unique lens through which to view a startup's valuation, grounding it in the reality of the market's historical willingness to pay.

Final Synthesis: Integrating Valuation Methods and Next Steps

In the journey through the various methods of startup valuation, we've uncovered a range of approaches, each offering unique insights. Now, it's time to bring these diverse perspectives together, synthesizing them into a coherent whole.

This consolidation will enable us to capture a more complete picture of a startup's worth. Let's begin this final phase with a closer look at how we can integrate these insights effectively.

Consolidating the Valuation Insights

Having explored various valuation methodologies, the final step involves integrating these insights into a unified valuation. This can be presented as either a single value or a valuation range.

To determine a singular valuation, calculate the mean or median of the various results obtained. For a valuation range, use the lowest and highest values from the different methods to define the low and high ends.

Additionally, incorporating a sensitivity table that displays all results can provide valuable insights into how the valuation might fluctuate based on different comparison points.

Additional Considerations for Mature Companies

For mature companies with positive earnings, the Price-to-Earnings (PE) ratio is another useful metric. This ratio can be calculated by dividing the company's market capitalization by its net income. In the case of publicly traded companies, dividing the share price by the Earnings Per Share (EPS) offers a similar perspective. This approach essentially scales the market cap and net income to the number of shares outstanding, offering a per-share valuation insight.

Understanding the Fluidity of Market-Based Valuations

It's important to recognize that the valuation multiples discussed here provide a relative, market-based valuation. When applying these to a startup or a mature business, keep in mind that your company’s value may fluctuate in tandem with the market benchmarks.

Alternative for Companies Without Depreciation or Amortization

In instances where companies do not have significant depreciation or amortization, the EBIT (Earnings Before Interest and Taxes) multiple can be a suitable alternative to the EBITDA multiple.

Concluding Thoughts

This post has delved into several valuation methods that leverage market data against a company's financial forecasts. I find these methods versatile and generally accurate across different business types and stages.

Now, I'd love to hear your thoughts. Did you find this deep dive into comparables valuation helpful? What topics would you like us to explore in future posts? Feel free to share your thoughts and suggestions in the comments below.

Key Takeaways

Versatility Across Stages: Suitable for any development stage, especially useful for pre-revenue and early-stage startups using revenue multiples.

Real Market Data Utilization: Elevates valuation discussions by incorporating actual financial ratios from peer companies, reflecting current investor valuations.

Comprehensive Benchmarking: Includes direct and indirect competitors, market leaders, and companies with similar business models for nuanced analysis.

Dual-Faceted Valuation for Maturity: Applies both revenue and EBITDA multiples for mature companies, offering a rounded assessment of business value.

Previous Transaction Insights: Grounds valuation in market realities by leveraging historical deal sizes and financial metrics, though data gathering can be challenging.

Answers to The Most Asked Questions

-

Estimating a company's value by comparing it to similar businesses in the same industry using financial ratios.

-

A method to estimate a company's value by comparing it with similar companies using metrics like revenue or EBITDA multiples.

-

DCF focuses on future cash flows discounted to present value; comparables use financial ratios of similar companies for valuation.

-

The process of determining the worth of a startup, considering factors like market potential and technological innovation.

-

To establish fair terms for equity sales during funding rounds and to reflect the startup's market position and potential growth.

-

Yes, especially useful for early-stage startups by applying revenue multiples from similar companies to estimate valuation.