Top 7 Startup Valuation Methods

By Lior Ronen | Founder, Finro Financial Consulting

Understanding how to value a tech startup is crucial for entrepreneurs and investors alike.

Unlike established businesses, tech startups require a different approach, focusing more on potential growth and future projections rather than just past performance.

This guide explores the most effective methods for valuing tech startups.

We'll cover the basics and delve into specific techniques, providing you with practical insights you can use to evaluate your own business or potential investments.

Startup valuation combines art and science.

It often works with limited data and emphasizes future possibilities, making the process both challenging and rewarding. By following this guide, you'll understand the common valuation methods and how to apply them in real-world scenarios.

Let’s jump in and start exploring the world of tech startup valuation.

Accurately valuing tech startups involves understanding their unique characteristics and using tailored methods like the Berkus, Payne Scorecard, VC, Multiples, and DCF methods. Early-stage startups benefit from qualitative approaches that emphasize potential and innovation, while late-stage startups require quantitative methods focused on financial performance.

Combining these methods provides a comprehensive valuation. Factors like development stage, industry specifics, and financial data availability are crucial in choosing the right approach. Finro offers personalized, cost-effective valuation services with rapid turnaround times, ensuring tech startups receive accurate valuations that reflect their true potential and support strategic growth.

- Understanding Startups

- What is Startup Valuation?

- The Berkus Method

- The Payne Scorecard Method

- The VC Method

- Multiples Method for Early-Stage Startups

- Using Previous Transactions

- Multiples Method for Late-Stage Startups

- Discounted Cash Flow (DCF) Method

- Choosing the Right Valuation Method

- Choosing Finro as Your Valuation Consultant

- Conclusion

Understanding Startups

Before discussing the specifics of valuing a tech startup, it’s important to understand what exactly constitutes a startup and how it differs from an established business.

This foundational understanding will help contextualize the unique challenges and opportunities of valuing new ventures.

Definition and Characteristics of a Startup

A startup is a young company founded to develop a unique product or service and bring it to market. Unlike traditional businesses, startups aim to innovate and disrupt existing markets with new solutions. Key characteristics of a startup include:

Innovation: Startups often focus on creating new products, services, or technologies that challenge the status quo.

Scalability: Startups are designed to grow rapidly, often with the potential to expand significantly with minimal incremental cost.

Flexibility: Startups are typically more agile and adaptable than established businesses, able to pivot quickly in response to market feedback.

Risk and Uncertainty: Startups operate in an environment of high uncertainty and risk, often relying on unproven business models and facing significant financial and operational challenges.

Differences Between Startups and Established Businesses

While both startups and established businesses aim to generate profit and provide value to customers, they differ in several key ways:

Stage of Development: Startups are in the early stages of development, focusing on innovation and market entry. Established businesses have a proven track record and stable operations.

Growth Strategy: Startups prioritize rapid growth and scalability, often seeking venture capital to fuel expansion. Established businesses focus on sustainable growth and maintaining market share.

Market Presence: Startups are typically new entrants in their market, working to build brand recognition and customer base. Established businesses have a well-known brand and a loyal customer base.

Organizational Structure: Startups usually have a flat, flexible organizational structure that encourages collaboration and quick decision-making. Established businesses tend to have more formal hierarchies and processes.

Resource Availability: Startups often operate with limited resources, relying on creativity and resourcefulness. Established businesses have access to significant financial, human, and operational resources.

Understanding these differences is crucial when valuing startups, as their unique characteristics and growth potential require different valuation approaches compared to established businesses.

| Aspect | Startup | Established Business |

|---|---|---|

| Stage of Development | Early stage, focusing on innovation and market entry | Proven track record, stable operations |

| Growth Strategy | Rapid growth and scalability | Sustainable growth, maintaining market share |

| Market Presence | New entrant, building brand recognition and customer base | Well-known brand, loyal customer base |

| Organizational Structure | Flat, flexible, encourages quick decision-making | Formal hierarchies, established processes |

| Resource Availability | Limited resources, relies on creativity and resourcefulness | Significant financial, human, and operational resources |

| Risk and Uncertainty | High risk and uncertainty, unproven business models | Lower risk, established business models |

What is Startup Valuation?

Before diving into the various methods of valuing a tech startup, it’s essential to understand what startup valuation entails, why it’s important, and the key factors that influence it.

This foundational knowledge will provide the context needed to appreciate the nuances of the different valuation techniques.

Explanation of Startup Valuation

Startup valuation is the process of determining the worth of a young company. Unlike traditional businesses, where valuation might rely heavily on past financial performance, startup valuation often hinges on future potential and projections.

This involves estimating the value of a startup's assets, including its intellectual property, customer base, and growth potential. The goal is to provide a realistic assessment of the startup's worth under various scenarios.

Importance of Startup Valuation

Understanding the value of a startup is crucial for several reasons:

Attracting Investors: Accurate valuation helps attract investors by providing a clear picture of the startup's potential. Investors need to know the company's worth before they commit their funds.

Raising Capital: A well-substantiated valuation can help raise capital by setting the groundwork for funding rounds. It helps founders negotiate better terms and secure the necessary resources for growth.

Strategic Planning: Knowing the startup’s value allows founders to make informed decisions about the future, including expansion plans, partnerships, and potential exits.

Employee Compensation: Valuation is also important for structuring employee compensation, especially when offering stock options or equity as part of the remuneration package.

Key Factors Influencing Startup Valuation

Several factors influence the valuation of a startup. Understanding these can help in creating a more accurate and compelling valuation:

Market Opportunity: The size and growth potential of the market the startup targets play a significant role. A larger market with high growth potential can lead to a higher valuation.

Business Model: The viability and scalability of the startup's business model are critical. Investors look for models that can generate significant revenue and profit over time.

Team Quality: The founding team's experience, skills, and track record are crucial. A strong team can execute the business plan effectively and adapt to challenges.

Technology and Product: The uniqueness, innovation, and stage of development of the startup's product or technology can greatly impact valuation. Products that solve a significant problem or offer a distinct competitive advantage are valued higher.

Revenue and Growth: Current revenue, growth rate, and future revenue projections are key indicators of a startup’s potential. High growth rates and clear paths to revenue generation are attractive to investors.

Competitive Landscape: The level of competition and the startup's positioning within the market influence valuation. A startup with a strong market position or a unique offering can command a higher valuation.

Risk Factors: Finally, the startup's overall risk profile, including market risks, operational risks, and financial risks, affects its valuation. Startups demonstrating effective risk management and mitigation strategies are valued more favorably.

Understanding these factors and their impact on valuation can help entrepreneurs present a compelling case to investors and other stakeholders.

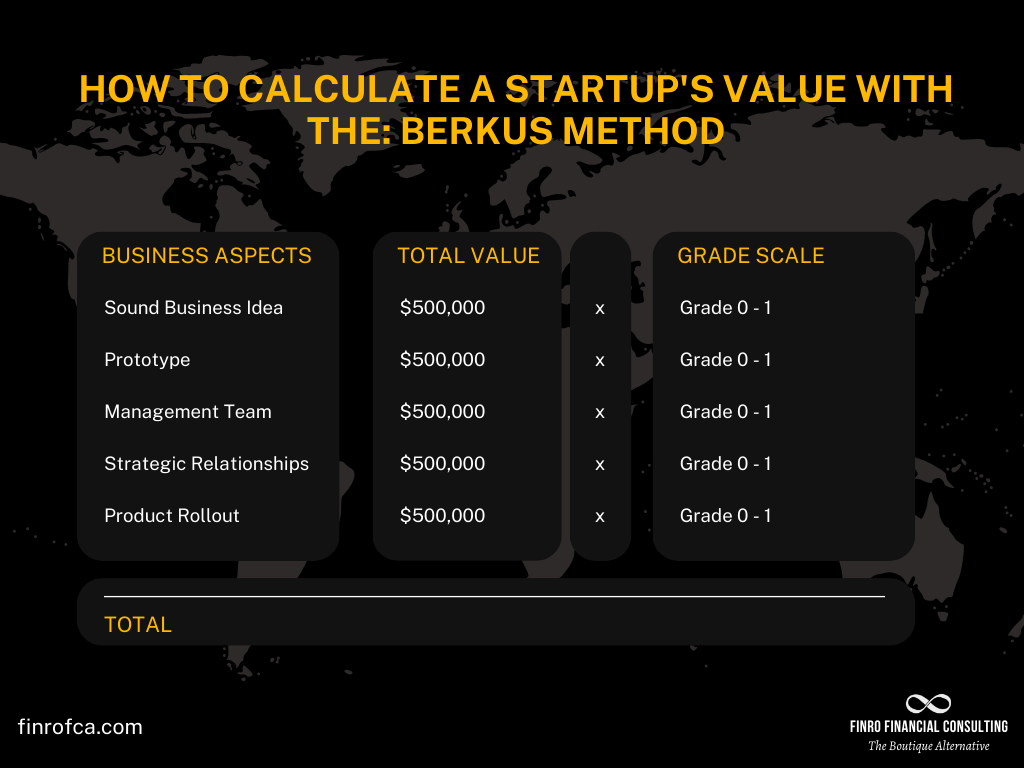

The Berkus Method

The Berkus Method is a straightforward and qualitative approach to valuing early-stage startups, especially those in the tech industry.

Developed by angel investor Dave Berkus, this method focuses on assessing a startup's inherent risks and potential by assigning monetary values to various qualitative factors.

How It Works

The Berkus Method evaluates a startup based on five key factors, each assigned a specific value of up to $500,000. The total valuation can reach up to $2.5 million. The factors are:

Sound Idea (Basic Value): Is there a viable idea or prototype? A strong concept or prototype can be valued up to $500,000.

Prototype (Reducing Technology Risk): Has the startup developed a working prototype? A functional prototype can add up to $500,000 to the valuation.

Quality Management Team (Reducing Execution Risk): Does the startup have a competent and experienced management team? A solid team can contribute up to $500,000.

Strategic Relationships (Reducing Market Risk): Are strategic partnerships or potential customer relationships in place? These relationships can add up to $500,000.

Product Rollout or Sales (Reducing Production Risk): Is there evidence of market traction, such as product rollout or initial sales? This can be valued up to $500,000.

Pros and Cons

Pros:

Simplicity: The Berkus Method is easy to understand and apply, making it accessible for founders and investors.

Qualitative Focus: This method emphasizes qualitative aspects, often crucial for early-stage startups without significant financial data.

Risk Mitigation: This method addresses different types of risks and provides a holistic view of the startup's potential.

Cons:

Subjectivity: The method relies on subjective judgments, which can vary between evaluators.

Limited Financial Insight: It doesn't account for detailed financial projections or market conditions.

Cap on Valuation: The $2.5 million cap may not reflect the potential of startups in highly lucrative markets.

Examples of Application

Tech Startup with a Strong Prototype: A tech startup with a viable prototype, a competent team, and initial strategic partnerships might be valued as follows:

Sound Idea: $400,000

Prototype: $450,000

Quality Management Team: $400,000

Strategic Relationships: $300,000

Product Rollout: $200,000

Total Valuation: $1,750,000

Early-Stage AI Company: An AI company with a groundbreaking idea but still in the development phase:

Sound Idea: $500,000

Prototype: $300,000

Quality Management Team: $350,000

Strategic Relationships: $200,000

Product Rollout: $0

Total Valuation: $1,350,000

These examples illustrate how the Berkus Method can be applied to different scenarios, providing a framework to evaluate the potential of early-stage startups.

The Payne Scorecard Method

The Payne Scorecard Method, developed by Bill Payne, is a systematic approach to valuing early-stage startups. It scores various factors that contribute to the company's potential success.

This method is particularly useful for angel investors as it offers a structured way to evaluate and compare startups based on weighted criteria.

How It Works

The Payne Scorecard Method involves the following steps:

Determine the Base Valuation: Start by identifying a comparable startup recently funded in the same industry and region. Use this as the base valuation.

Assign Weight to Key Factors: Evaluate the startup across several key factors, assigning a percentage weight based on their relative importance. The typical factors include:

Strength of the Management Team (0-30%)

Size of the Opportunity (0-25%)

Product/Technology (0-15%)

Competitive Environment (0-10%)

Marketing/Sales Channels/Partnerships (0-10%)

Need for Additional Investment (0-5%)

Other Factors (0-5%)

Score the Startup: For each factor, assign a score based on how well the startup performs relative to the comparable company. The score ranges from 0 to 1, where 1 means the startup matches the comparable, and lower scores indicate lesser performance.

Calculate the Adjusted Valuation: Multiply the base valuation by the total weighted score to get the startup’s adjusted valuation.

Pros and Cons

Pros:

Structured Approach: The method provides a clear, structured way to evaluate startups, making it easier to compare different companies.

Comprehensive Evaluation: The method offers a holistic view of the startup’s potential by considering multiple factors.

Flexibility: The weights can be adjusted based on the specific industry or investor preferences.

Cons:

Subjectivity: Assigning scores and weights involves subjective judgment, which can lead to variability in valuations.

Dependence on Comparable Data: Finding a comparable startup can be challenging, and the base valuation may not always be accurate.

Complexity: The method is more complex than other valuation techniques, requiring detailed analysis and comparison.

Examples of Application

Fintech Startup: A fintech startup is being compared to a recently funded company with a base valuation of $2 million. The evaluation might look like this:

Strength of the Management Team: 0.8 (weight 30%)

Size of the Opportunity: 0.9 (weight 25%)

Product/Technology: 0.7 (weight 15%)

Competitive Environment: 0.6 (weight 10%)

Marketing/Sales Channels/Partnerships: 0.8 (weight 10%)

Need for Additional Investment: 0.5 (weight 5%)

Other Factors: 0.7 (weight 5%)

Total Score: (0.8 * 30%) + (0.9 * 25%) + (0.7 * 15%) + (0.6 * 10%) + (0.8 * 10%) + (0.5 * 5%) + (0.7 * 5%) = 0.765

Adjusted Valuation: $2,000,000 * 0.765 = $1,530,000

Healthcare Startup: A healthcare startup is being compared to a similar company with a base valuation of $3 million:

Strength of the Management Team: 0.9 (weight 30%)

Size of the Opportunity: 1.0 (weight 25%)

Product/Technology: 0.8 (weight 15%)

Competitive Environment: 0.7 (weight 10%)

Marketing/Sales Channels/Partnerships: 0.9 (weight 10%)

Need for Additional Investment: 0.6 (weight 5%)

Other Factors: 0.8 (weight 5%)

Total Score: (0.9 * 30%) + (1.0 * 25%) + (0.8 * 15%) + (0.7 * 10%) + (0.9 * 10%) + (0.6 * 5%) + (0.8 * 5%) = 0.865

Adjusted Valuation: $3,000,000 * 0.865 = $2,595,000

These examples illustrate how the Payne Scorecard Method can be applied to different startups, providing a structured way to adjust the base valuation based on the startup’s unique attributes.

Get your expert support now!

The VC Method

The Venture Capital (VC) Method is a popular approach used by venture capitalists to value early-stage startups.

This method focuses on the expected return on investment (ROI) and typically involves calculating the startup's post-money valuation based on its projected future value at exit.

How It Works

The VC Method involves several key steps:

Estimate the Exit Value: Determine the potential future value of the startup at the time of exit, usually based on projected revenues or earnings and applying a market multiple.

Determine the Desired ROI: Decide on the target return on investment, which is usually high due to the risk associated with early-stage investments. VCs often look for returns in the range of 10x to 30x their initial investment.

Calculate the Post-Money Valuation: Divide the estimated exit value by the desired ROI to get the post-money valuation.

Determine the Pre-Money Valuation: Subtract the amount of new investment from the post-money valuation to obtain the pre-money valuation.

Pros and Cons

Pros:

Focus on Returns: The method aligns with investors’ primary goal of achieving high returns on their investments.

Future-Oriented: By considering the potential future value, the method takes into account the growth potential of the startup.

Simplicity: The VC Method is relatively straightforward and easy to understand.

Cons:

High Uncertainty: Estimating the future exit value involves a high degree of uncertainty and speculation.

Market Dependence: The method relies on market multiples, which can fluctuate and may not accurately reflect the startup’s value.

Investor-Centric: The method focuses more on investor returns rather than the intrinsic value of the startup, which can sometimes lead to undervaluation from the founder's perspective.

Examples of Application

SaaS Startup: A SaaS startup projects to achieve $50 million in revenue in 5 years. The average market multiple for similar companies is 5x revenue. The VC desires a 20x return on investment.

Estimated Exit Value: $50 million * 5 = $250 million

Desired ROI: 20x

Post-Money Valuation: $250 million / 20 = $12.5 million

Pre-Money Valuation: If the VC invests $2.5 million, the pre-money valuation is $12.5 million - $2.5 million = $10 million

E-commerce Startup: An e-commerce startup projects to achieve $30 million in earnings in 7 years. The average market multiple for similar companies is 8x earnings. The VC desires a 15x return on investment.

Estimated Exit Value: $30 million * 8 = $240 million

Desired ROI: 15x

Post-Money Valuation: $240 million / 15 = $16 million

Pre-Money Valuation: If the VC invests $4 million, the pre-money valuation is $16 million - $4 million = $12 million

These examples show how the VC Method can be applied to different types of startups, providing a clear framework for investors to assess the potential return on their investment based on future projections.

Multiples Method for Early-Stage Startups

The multiples method is widely used to valuing early-stage startups by comparing them to similar private companies.

This method uses financial metrics, such as revenue, to determine a startup’s value.

For early-stage startups, revenue multiples are often the most relevant.

How It Works

The multiples method involves the following steps:

Identify Comparable Companies: Find similar private startups within the same industry and growth stage. These companies should have similar business models, market conditions, and revenue streams.

Calculate the Revenue Multiple: Determine the revenue multiple by dividing the valuation of comparable companies by their revenue. For example, if a comparable company is valued at $10 million and has $2 million in revenue, the revenue multiple is 5x.

Apply the Revenue Multiple: Multiply the startup's revenue by the determined multiple to estimate its valuation.

Pros and Cons

Pros:

Simplicity: The method is straightforward and easy to understand.

Market-Based: Reflects current market conditions and investor sentiment.

Scalability: Suitable for early-stage startups with limited financial data.

Cons:

Subjectivity: Finding truly comparable companies can be subjective and challenging.

Market Fluctuations: Market conditions can change, affecting the relevance of the multiple.

Limited Financial Insight: Doesn't consider future growth potential or profitability.

Examples of Application

SaaS Startup: A SaaS startup generates $1 million in annual revenue. Comparable SaaS companies have a revenue multiple of 6x.

Revenue Multiple: 6x

Startup Revenue: $1 million

Estimated Valuation: $1 million * 6 = $6 million

E-commerce Startup: An e-commerce startup generates $500,000 in annual revenue. Comparable e-commerce startups have a revenue multiple of 4x.

Revenue Multiple: 4x

Startup Revenue: $500,000

Estimated Valuation: $500,000 * 4 = $2 million

Fintech Startup: A fintech startup generates $2 million in annual revenue. Comparable fintech companies have a revenue multiple of 5x.

Revenue Multiple: 5x

Startup Revenue: $2 million

Estimated Valuation: $2 million * 5 = $10 million

These examples demonstrate how the multiples method can be applied to early-stage startups, providing a practical way to estimate their value based on comparable companies' revenue multiples.

This approach helps investors and entrepreneurs understand the market value of a startup relative to its peers.

Using Previous Transactions

Past deal data plays a critical role in valuing early-stage startups. By analyzing the valuations of similar companies in previous transactions, entrepreneurs and investors can gain insights into current market trends and benchmarks. This data helps to:

Benchmark Valuations: Understand the market standards for valuing similar startups.

Negotiate Better Deals: Use historical data to justify valuations during investment discussions.

Identify Market Trends: Detect trends and shifts in how investors value startups over time.

How to Apply the Multiples Method Using Previous Transactions

Applying the multiples method using past transaction data involves several steps:

Collect Relevant Data: Gather data on previous transactions involving similar startups. This includes information on the company's industry, stage of development, revenue, and the valuation at which they were funded or acquired.

Calculate Transaction Multiples: Determine the revenue multiples from these past transactions. This is done by dividing the transaction valuation by the company's revenue at the time of the deal.

Example: If a startup was acquired for $8 million and had $2 million in revenue, the transaction multiple is 4x.

Determine an Average Multiple: Calculate the average revenue multiple from the collected data. This average will serve as a benchmark for valuing the current startup.

Example: If similar transactions have multiples of 4x, 5x, and 6x, the average multiple is (4 + 5 + 6) / 3 = 5x.

Apply the Average Multiple: Multiply the current startup's revenue by the average multiple to estimate its valuation.

Example: If the startup has $1.5 million in revenue and the average multiple is 5x, the valuation is $1.5 million * 5 = $7.5 million.

Examples and Case Studies

HealthTech Startup: A HealthTech startup with $3 million in annual revenue. Previous transactions in the HealthTech sector show an average revenue multiple of 7x.

Transaction Multiples: 6x, 7x, 8x

Average Multiple: (6 + 7 + 8) / 3 = 7x

Estimated Valuation: $3 million * 7 = $21 million

EdTech Startup: An EdTech startup with $2 million in annual revenue. Similar EdTech startups were funded with an average revenue multiple of 4.5x.

Transaction Multiples: 4x, 4.5x, 5x

Average Multiple: (4 + 4.5 + 5) / 3 = 4.5x

Estimated Valuation: $2 million * 4.5 = $9 million

GreenTech Startup: A GreenTech startup with $1 million in annual revenue. Historical data shows an average revenue multiple of 6x for comparable companies.

Transaction Multiples: 5.5x, 6x, 6.5x

Average Multiple: (5.5 + 6 + 6.5) / 3 = 6x

Estimated Valuation: $1 million * 6 = $6 million

By leveraging past transaction data, startups can align their valuations with market expectations and provide a solid basis for negotiations with investors.

This method helps ensure that valuations are realistic and grounded in real-world examples, facilitating more effective and transparent discussions.

Multiples Method for Late-Stage Startups

After introducing the multiples method for early-stage startups, we now focus on its variation for late-stage startups.

For late-stage startups, the multiples method leverages more established financial performance metrics such as revenue and EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization).

These companies typically have consistent revenue and profitability, making comparing them to similar private companies easier.

Revenue Multiples for Private Companies

Revenue multiples are calculated by comparing a company's revenue to its valuation. For late-stage startups, revenue multiples can be a reliable indicator of value, especially when there is consistent and significant revenue generation.

Determine Comparable Companies: Identify late-stage startups in the same industry and with similar business models.

Calculate Revenue Multiple: Divide the valuation of these comparable companies by their revenue.

Example: If a comparable company is valued at $50 million and has $10 million in revenue, the revenue multiple is 5x.

Apply the Multiple: Multiply the subject startup's revenue by the derived multiple.

Example: If the subject startup has $15 million in revenue and the average revenue multiple is 5x, its valuation would be $15 million * 5 = $75 million.

EBITDA Multiples for Private Companies

EBITDA multiples consider a company’s operating performance and profitability, making them useful for valuing late-stage startups that are closer to profitability or already profitable.

Identify Comparable Companies: Find late-stage private companies with similar EBITDA figures in the same industry.

Calculate EBITDA Multiple: Divide the valuation of these companies by their EBITDA.

Example: If a comparable company is valued at $60 million and has an EBITDA of $12 million, the EBITDA multiple is 5x.

Apply the Multiple: Multiply the subject startup's EBITDA by the derived multiple.

Example: If the subject startup has an EBITDA of $8 million and the average EBITDA multiple is 5x, its valuation would be $8 million * 5 = $40 million.

Application Examples

Fintech Startup: A late-stage fintech startup has $20 million in annual revenue and $4 million in EBITDA. Comparable fintech companies have an average revenue multiple of 6x and an EBITDA multiple of 8x.

Revenue Multiple Valuation: $20 million * 6 = $120 million

EBITDA Multiple Valuation: $4 million * 8 = $32 million

Final Valuation: The higher of the two valuations may be used, or an average can be taken depending on investor preference. Here, $120 million (revenue-based) or $32 million (EBITDA-based).

HealthTech Startup: A HealthTech startup with $10 million in annual revenue and $3 million in EBITDA. Comparable companies have an average revenue multiple of 7x and an EBITDA multiple of 10x.

Revenue Multiple Valuation: $10 million * 7 = $70 million

EBITDA Multiple Valuation: $3 million * 10 = $30 million

Final Valuation: $70 million (revenue-based) or $30 million (EBITDA-based).

E-commerce Startup: An e-commerce startup with $25 million in annual revenue and $5 million in EBITDA. Comparable e-commerce companies have an average revenue multiple of 4x and an EBITDA multiple of 6x.

Revenue Multiple Valuation: $25 million * 4 = $100 million

EBITDA Multiple Valuation: $5 million * 6 = $30 million

Final Valuation: $100 million (revenue-based) or $30 million (EBITDA-based).

Using this variation of the multiples method for late-stage startups allows investors and entrepreneurs to derive valuations based on established financial performance and industry benchmarks, providing a clear and market-aligned estimate of the company's worth.

Discounted Cash Flow (DCF) Method

The Discounted Cash Flow (DCF) method is a valuation technique that estimates a startup's value based on its expected future cash flows.

This method involves forecasting the company’s free cash flows (FCF) and discounting them back to their present value using the Weighted Average Cost of Capital (WACC).

The DCF method is particularly useful for late-stage startups with more predictable cash flows.

Key Components

Free Cash Flow (FCF): The cash generated by the company after accounting for operating expenses, capital expenditures, and changes in working capital. It represents the cash available to all investors, both equity and debt holders.

Weighted Average Cost of Capital (WACC): The average rate of return required by all of the company’s investors. It reflects the cost of equity and debt financing.

Terminal Value: The value of the startup’s cash flows beyond the forecast period, extending into perpetuity. It accounts for the majority of the valuation in most DCF analyses.

Net Present Value (NPV): The sum of the present values of the forecasted FCFs and the terminal value, discounted by the WACC. It represents the estimated value of the startup.

Step-by-Step Guide to Calculating DCF

Project Free Cash Flows: Forecast the startup’s FCF for a specific period (e.g., 5-10 years).

Example: Projected FCF for Year 1: $1 million, Year 2: $2 million, Year 3: $3 million, etc.

Calculate the Terminal Value: Use the perpetuity growth model or exit multiple method to estimate the terminal value.

Example: Terminal Value = FCF in Final Year * (1 + Growth Rate) / (WACC - Growth Rate). If the FCF in the final year is $5 million, the growth rate is 3%, and the WACC is 10%, then Terminal Value = $5 million * (1 + 0.03) / (0.10 - 0.03) = $5.15 million / 0.07 = $73.57 million.

Determine the WACC: Calculate the WACC based on the cost of equity and debt and their respective weights in the company’s capital structure.

Example: If the cost of equity is 12%, the cost of debt is 6%, and the debt-to-equity ratio is 1:1, then WACC = (0.5 * 12%) + (0.5 * 6%) = 9%.

Discount the FCFs and Terminal Value: Discount the forecasted FCFs and terminal value back to their present values using the WACC.

Example: Present Value of Year 1 FCF = $1 million / (1 + 0.09)^1 = $0.92 million, Present Value of Terminal Value = $73.57 million / (1 + 0.09)^5 = $47.74 million.

Calculate the NPV: Sum the present values of the forecasted FCFs and the terminal value to get the NPV.

Example: NPV = Present Value of Year 1 FCF + Present Value of Year 2 FCF + ... + Present Value of Terminal Value.

Application Examples

Fintech Startup: A fintech startup projects the following FCFs: Year 1: $2 million, Year 2: $3 million, Year 3: $4 million, Year 4: $5 million, Year 5: $6 million. The terminal value is $90 million, and the WACC is 10%.

Discounted FCFs: Year 1: $1.82 million, Year 2: $2.48 million, Year 3: $3.00 million, Year 4: $3.41 million, Year 5: $3.73 million.

Discounted Terminal Value: $90 million / (1 + 0.10)^5 = $55.92 million.

NPV: $1.82 million + $2.48 million + $3.00 million + $3.41 million + $3.73 million + $55.92 million = $70.36 million.

HealthTech Startup: A HealthTech startup forecasts the following FCFs: Year 1: $1 million, Year 2: $1.5 million, Year 3: $2 million, Year 4: $2.5 million, Year 5: $3 million. The terminal value is $50 million, and the WACC is 8%.

Discounted FCFs: Year 1: $0.93 million, Year 2: $1.29 million, Year 3: $1.59 million, Year 4: $1.84 million, Year 5: $2.04 million.

Discounted Terminal Value: $50 million / (1 + 0.08)^5 = $34.25 million.

NPV: $0.93 million + $1.29 million + $1.59 million + $1.84 million + $2.04 million + $34.25 million = $41.94 million.

Using the DCF method allows investors and entrepreneurs to derive a valuation based on the expected future financial performance of the startup, providing a detailed and forward-looking estimate of the company's worth.

Choosing the Right Valuation Method

Selecting the appropriate valuation method for a startup depends on several key factors. These factors help determine the most suitable approach for providing an accurate and realistic valuation:

Stage of Development: The maturity of the startup (early-stage vs. late-stage) influences which methods are most applicable. Early-stage startups may rely more on qualitative methods, while late-stage startups can use quantitative approaches.

Industry: Different industries have varying norms and benchmarks for valuation. Understanding industry-specific factors can guide the choice of method.

Financial Data Availability: The availability and reliability of financial data impact the choice. For example, the DCF method requires detailed financial projections, while the Berkus Method relies on qualitative assessments.

Risk Profile: Startups with higher uncertainty and risk may benefit from methods that account for qualitative factors, while more stable startups can use quantitative methods.

Investor Preferences: Potential investors' preferences and requirements can also influence the choice of valuation method. Some investors may prefer certain methods over others.

When to Use Each Method

Each valuation method has its strengths and is suited for specific scenarios:

Berkus Method:

Use When: The startup is in the very early stages, with minimal financial data available.

Best For: Tech startups with strong ideas and prototypes but little to no revenue.

Payne Scorecard Method:

Use When: You need a structured approach to evaluate multiple qualitative factors.

Best For: Early-stage startups where qualitative aspects such as team quality and market opportunity are crucial.

VC Method:

Use When: The startup has potential for high growth, and you need to estimate returns for investors.

Best For: Startups seeking venture capital with high expected ROI.

Multiples Method for Early-Stage Startups:

Use When: There are comparable private companies and a limited financial history.

Best For: Early-stage startups with some revenue but not enough for detailed projections.

Using Previous Transactions:

Use When: Data on recent deals involving similar companies is available.

Best For: Startups in industries with frequent transactions providing useful benchmarks.

Multiples Method for Late-Stage Startups:

Use When: The startup has significant revenue or EBITDA, and there are comparable companies.

Best For: Late-stage startups with established financial performance.

Discounted Cash Flow (DCF) Method:

Use When: The startup has reliable financial projections and a clear path to profitability.

Best For: Late-stage startups with predictable cash flows and detailed financial forecasts.

Combining Methods for a More Accurate Valuation

Combining multiple methods can be beneficial to achieve a more accurate and comprehensive valuation. Here’s how to approach it:

Blend Qualitative and Quantitative Approaches: Use qualitative methods (e.g., Berkus, Payne Scorecard) to capture the startup’s potential and team quality, and quantitative methods (e.g., Multiples, DCF) to assess financial performance and market positioning.

Cross-Validate Results: Apply different methods and compare the results to identify discrepancies and validate the findings. This helps in cross-checking assumptions and ensures robustness.

Adjust for Specific Factors: Consider industry-specific factors and unique aspects of the startup to adjust the valuation. This tailored approach can refine the overall estimate.

Consult with Experts: Engage with industry experts, investors, and financial advisors to gain insights and refine the valuation. Their perspectives can help balance optimistic projections with market realities.

By considering these factors and strategically combining methods, entrepreneurs and investors can arrive at a well-rounded and reliable valuation that reflects the true potential and worth of the startup.

Choosing Finro as Your Valuation Consultant

Navigating the complexities of tech startup valuation requires more than a standard approach; it demands a partner who understands the unique challenges and opportunities that tech startups face. This is where Finro steps in.

Finro offers tailored valuation services beyond traditional methods, ensuring that every aspect of your startup's value is accurately captured and effectively communicated. Our approach is designed to provide tech startups with the precise and actionable insights needed to attract investors, drive growth, and achieve long-term success.

At Finro, we recognize that every tech startup is unique, with its own business model, market dynamics, and growth trajectory. Our team of experienced professionals takes the time to understand your startup's specific needs and goals thoroughly.

We develop a customized valuation that reflects your startup's potential by diving deep into your financial data, market conditions, and competitive landscape. This personalized attention ensures that our valuation is accurate and meaningful, helping you make informed strategic decisions and present a compelling case to investors.

Moreover, Finro's commitment to delivering high-quality, cost-effective solutions differentiates us from traditional valuation services. We understand the financial pressures that tech startups face and strive to offer our services at competitive prices without compromising on quality. Additionally, our efficient processes and rapid turnaround times mean you won't be left waiting for months to receive vital valuation figures.

With Finro, you gain a strategic partner who is dedicated to your success, providing you with the expert guidance and support needed to navigate the financial complexities of the tech startup world confidently. Choose Finro to unlock the true value of your tech startup and propel it toward lasting success.

Conclusion

Navigating the complexities of tech startup valuation requires a nuanced approach that appreciates the unique challenges and opportunities inherent in the tech industry. Throughout this guide, we’ve explored various valuation methods, each tailored to different stages and aspects of startup development.

From the Berkus and Payne Scorecard Methods for early-stage startups to the Multiples and DCF Methods for late-stage startups, understanding these approaches empowers entrepreneurs and investors to make informed decisions and accurately assess the value of their ventures.

Choosing the right valuation method is crucial, and often a combination of methods yields the most accurate results. By considering factors such as the stage of development, industry specifics, financial data availability, and investor preferences, you can select and apply the most appropriate techniques for your startup.

This strategic approach ensures that valuations are not just numbers but tools that reflect the true potential and worth of your business.

For those seeking a more tailored and strategic valuation service, Finro stands out as the ideal partner. Finro’s expertise in tech startup valuations, combined with personalized attention, cost-effective solutions, and rapid turnaround times, makes us a valuable ally in your growth journey.

Our commitment to understanding your unique business needs and delivering actionable insights ensures that you are well-equipped to attract investors and achieve your strategic goals.

In conclusion, whether you are an entrepreneur looking to attract funding or an investor seeking to understand the value of a potential investment, mastering the art and science of startup valuation is essential.

Partnering with experts like Finro can provide the guidance and precision needed to navigate this complex landscape successfully. Together, let’s unlock the true value of your tech startup and propel it towards lasting success.

Key Takeaways

Tailored Methods: Use specific valuation methods suited to startup stages for accurate assessments.

Combine Techniques: Blend qualitative and quantitative approaches for comprehensive valuations.

Key Factors: Consider the development stage, industry, data, and investor needs when choosing valuation methods.

Finro Advantage: Finro provides personalized, cost-effective, and rapid valuation services for tech startups.

Strategic Partnership: Partnering with Finro ensures accurate valuations and strategic growth support.